We at Crack4sure are committed to giving students who are preparing for the AHIP AHM-520 Exam the most current and reliable questions . To help people study, we've made some of our Health Plan Finance and Risk Management exam materials available for free to everyone. You can take the Free AHM-520 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

The medical loss ratio (MLR) for the Peacock health plan is 80%. Peacock's expense ratio is 16%.

One characteristic of Peacock's MLR is that it

A health plan can use cost accounting in order to

The sentence below contains two pairs of terms enclosed in parentheses.

Determine which term in each pair correctly completes the statement. Then select the answer choice containing the two terms that you have selected. In analyzing its financial data, a health plan would use (horizontal/common size financial statement) analysis to measure the numerical amount that corresponding items change from one financial statement to another over consecutive accounting periods, and the health plan would use (trend/vertical) analysis to show the relationship of each financial statement item to another financial statement item.

The medical loss ratio (MLR) for the Peacock health plan is 80%. Peacock's expense ratio is 16%.

Peacock's MLR and its expense ratio indicate that Peacock

Mandated benefit laws are state or federal laws that require health plans to arrange for the financing and delivery of particular benefits. Ways that mandated benefits have the potential to influence health plans include:

1. Causing a lower degree of uniformity among health plans of competing health plans in a given market

2. Increasing the cost of the benefit plan to the extent that the plan must cover mandated benefits that would not have been included in the plan in the absence of the law or regulation that mandates the benefits

Dr. Jacob Winburne is compensated by the Honor Health Plan under an arrangement in which Honor establishes at the beginning of a financial period a fund from which claims approved for payment are paid. At the end of the given period, any funds remaining are paid out to providers. This information indicates that the arrangement between Dr. Winburne and Honor includes a provider incentive known as a:

Residual trend is the difference between total trend and the portion of the total trend caused by changes in provider reimbursement levels.

Consider the following events that could affect an health plan’s provider reimbursement levels:

Event 1 — The disenrollment of a large group with unusually high utilization rates

Event 2 — The introduction of a new treatment for infertility

Event 3 — A serious flu epidemic

Event 4 — A shift in inpatient medical services from obstetrical care to neonatal intensive care

One cause of residual trend is change in intensity, which would be represented by:

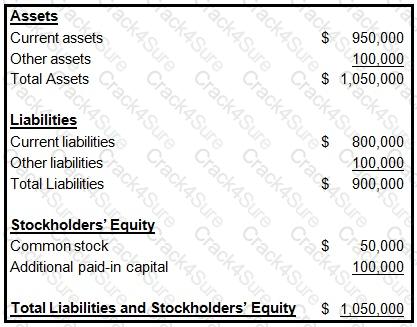

The following information was presented on one of the financial statements prepared by the Rouge health plan as of December 31, 1998:

When calculating its cash-to-claims payable ratio, Rouge would correctly divide its:

Julio Benini is eligible to receive healthcare coverage through a health plan that is under contract to his employer. Mr. Benini is seeking coverage for the following individuals:

The health plan most likely would consider that the definition of a dependent, for purposes of healthcare coverage, applies to:

In a fee-for-service (FFS) reimbursement method, providers are paid per treatment or per service that they provide. One typical benefit of FFS reimbursement is that it:

The Proform Health Plan uses agents to market its small group business. Proform capitalizes the commission expense relating to this line of business by spreading the commissions over the premium-paying period of the healthcare coverage. This approach to expense recognition is known as:

The Nuevo health plan's capital structure consists of 30% debt and 70% equity. Nuevo's average after-tax cost of debt is 6% and its cost of equity is 12%. The following statement(s) can correctly be made about Nuevo's weighted average cost of capital (WACC):

Ways in which a company can increase its return on investment (ROI) include:

1. Reducing expenses to increase operating income

2. Increasing controllable investment

An investor deposited $1,000 in an interest-bearing account today. That sum will accumulate to $1,200 two years from now. One true statement about this transaction is that:

Providing services under Medicare or Medicaid can impose on health plans financial risks and costs that are greater than those related to providing services to the commercial population. Reasons that an health plan's financial risks and costs for providing services to Medicare and Medicaid enrollees tend to be higher include

The Violin Company offers its employees a triple option of health plans: an HMO, an HMO with a point of service (POS) option, and an indemnity plan.

Premiums are lowest for the HMO option and highest for the indemnity plan. Violin employees who anticipate that they will be individual low utilizes of healthcare services are most likely to enroll in the

With regard to a health plan's underwriting of groups, it can correctly be stated that, generally, a

The following information relates to the Hardcastle Health Plan for the month of June:

This information indicates that Hardcastle’s medical loss ratio (MLR) for the month of June was approximately equal to:

The Northwest Company offers its employees the option of choosing to receive their healthcare benefits from an HMO or from a traditional indemnity plan. The premiums for the HMO are lower than for the traditional indemnity plan. In this situation, it is correct to assume that:

1. Individual low utilizers are more likely to enroll in the traditional indemnity plan

2. Individual high utilizers are more likely to enroll in the HMO

A primary reason that a financial analyst would measure the Tapestry health plan's return on assets (ROA) is to determine the

The Montvale Health Plan purchased a piece of real estate 20 years ago for $40,000. It recently sold the real estate for $80,000 and reported a capital gain of $40,000 on this sale. Even though the purchasing power of the dollar declined by half during this period and Montvale realized no actual gain in purchasing power, Montvale recorded in its accounting records the $40,000 gain from this sale. This situation best illustrates the accounting concept known as the:

A health plan can use a SWOT (strengths, weaknesses, opportunities, and threats) analysis to analyze its relationships with the major providers in each market in which it conducts business.

The Wallaby Health Plan purchased an asset two years ago for $50,000. At the time of purchase, the asset had an appraised value of $52,000. The asset carries a value on Wallaby’s general ledger of $47,000, and its current market value is $80,000. According to the cost concept, Wallaby would report on its financial statements a value for this asset equal to:

The Harp Company self-funds the health plan for its employees. The plan is administered under a typical administrative-services-only (ASO) arrangement. One true statement about this ASO arrangement is that

The Essential Health Plan markets a product for which it assumed total expenses to equal 92% of premiums. Actual data relating to this product indicate that expenses equal 89% of premiums. This information indicates that the expense margin for this product has:

In order to achieve its goal of improved customer service, the Evergreen Health Plan will add three new customer service representatives to its existing staff, install a new switching station, and install additional phone lines. In this situation, the cost that would be classified as a sunk cost, rather than a differential cost, is the expense associated with:

In the following paragraph, a sentence contains two pairs of words enclosed in parentheses. Determine which word in each pair correctly completes the sentence. Then select the answer choice containing the two words that you have selected.

Budgeting approaches can be classified as static or flexible budgets, or as rolling or period budgets. A health plan most likely would use a (static / flexible) budget when a budget's objective is to reduce or limit expenses, and the health plan most likely would use a (rolling / period) budget if it would like to continually maintain projections for a certain time period into the future.

Health plans have access to a variety of funding sources depending on whether they are operated as for-profit or not-for-profit organizations. The Verde Health Plan is a for-profit health plan and the Noir Health Plan is a not-for-profit health plan. From the answer choices below, select the response that correctly identifies whether funds from debt markets and equity markets are available to Verde and Noir:

The Longview Hospital contracted with the Carlyle Health Plan to provide inpatient services to Carlyle’s enrolled members. Carlyle provides Longview with a type of stop-loss coverage that protects, on a claims incurred and paid basis, against losses arising from significantly higher than anticipated utilization rates among Carlyle’s covered population. The stop-loss coverage specifies an attachment point of 130% of Longview’s projected $2,000,000 costs of treating Carlyle plan members and requires Longview to pay 15% of any costs above the attachment point. In a given plan year, Longview incurred covered costs totaling $3,000,000.

With regard to the type of stop-loss coverage provided to Longview by Carlyle and to whether this coverage is classified as insurance or reinsurance, the risk transfer approach used in this situation can be described as:

Advantages to a company that elects to self-fund and to administer all aspects of its healthcare benefit plan include:

The Arista Health Plan is evaluating the following four groups that have applied for group healthcare coverage:

With respect to the relative degree of risk to Arista represented by these four companies, the company that would most likely expose Arista to the lowest risk is the:

The types of financial risks and costs to which a health plan is subject depends on whether the health plan provides services to the Medicare and/or Medicaid populations or to the commercial population. One distinction between providing services to the Medicare and Medicaid populations and to the commercial population is that Medicare and Medicaid enrollees typically:

The methods of alternative funding for health coverage can be divided into the following general categories:

Typically, small employers are able to use some of the alternative funding methods in

Federal law addresses the relationship between Medicare- or Medicaid contracting health plans and providers who are at "substantial financial risk."

Under federal law, Medicare- or Medicaid-contracting health plans

Because a health plan cannot decline coverage for individuals who are eligible for conversion of group health coverage to individual health coverage, the bulk of the health plan's underwriting for conversion policies is accomplished through health plan design.

The Health Maintenance Organization (HMO) Model Act, developed by the National Association of Insurance Commissioners (NAIC), represents one approach to developing solvency standards. One drawback to this type of solvency regulation is that it

A key factor that distinguishes the various types of health plans is the type and amount of risk that a health plan assumes with respect to the delivery and financing of healthcare benefits. An example of a type of health plan that typically assumes the financial risk of delivering and financing healthcare benefits is a

In order to calculate a simple monthly capitation payment, the Argyle Health Plan used the following information:

Given this information, Argyle would correctly calculate that the per member per month (PMPM) capitation rate should be

The Caribou health plan is a for-profit organization. The financial statements that Caribou prepares include balance sheets, income statements, and cash flow statements. To prepare its cash flow statement, Caribou begins with the net income figure as reported on its income statement and then reconciles this amount to operating cash flows through a series of adjustments. Changes in Caribou's cash flow occur as a result of the health plan's operating activities, investing activities, and financing activities.

To prepare its cash flow statement, Caribou uses the direct method rather than the indirect method.

The Lighthouse health plan operates in a state that allows the health plan to use an underwriting method of determining a group's premium in which underwriters treat several small groups as one large group for risk assessment purposes. This method, which helps Lighthouse more accurately estimate a small group's probable claims costs, is known as

The following statements are about a health plan's underwriting of small groups. Select the answer choice containing the correct statement.

The McGwire Health Plan is a for-profit health plan that issues stock. Events that will cause the owners' equity account of McGwire to change include

Over time, health plans and their underwriters have gathered increasingly reliable information about the morbidity experience of small groups.

Generally, in comparison to large groups, small groups tend to

With regard to the Medicaid program in the United States, it can correctly be stated that

Experience rating and manual rating are two rating methods that the Cheshire health plan uses to determine its premium rates. One difference between these two methods is that, under experience rating, Cheshire

Under the alternative funding method used by the Trilogy Company, the insurer charges Trilogy an initial premium that is based on the assumption that claims will be 93% of the expected claims for the year. If claims exceed 93% of expected claims, then Trilogy must reimburse the insurer for any additional claims paid, up to 112% of expected claims. The insurer bears the responsibility for paying claims in excess of 112% of expected claims.

From the following answer choices, choose the name of the alternative funding method described.

The Kayak Company self funds the health plan for its employees. This plan is an example of a type of self-funded plan known as a general asset plan. The fact that this is a completely self-funded plan indicates that

The Poplar Company and a Blue Cross/Blue Shield organization have contracted to provide a typical fully funded health plan for Poplar's employees. One true statement about this health plan for Poplar's employees is that

The following paragraph contains an incomplete statement. Select the answer choice containing the term that correctly completes the statement. Health plans face four contingency risks (C-risks): asset risk (C-1), pricing risk (C-2), interest-rate risk (C-3), and general management risk (C-4). Of these risks, ________________ is typically the most important risk that health plans face. This is true because a sizable portion of the total expenses and liabilities faced by a health plan come from contractual obligations to pay for future medical costs, and the exact amount of these costs is not known when the healthcare coverage is priced.

Under the alternative funding method used by the Flair Company, Flair assumes financial responsibility for paying claims up to a specified level and deposits the funds necessary to pay these claims into a bank account that belongs to Flair. However, an insurer, which acts as an agent of Flair, makes the actual payment of claims from this account. When claims exceed the specified level, the insurer pays the balance from its own funds. No state premium tax is levied on the amounts that Flair deposits into this bank account.

From the following answer choices, choose the name of the alternative funding method described.

The following statements illustrate common forms of capitation:

1. The Antler Health Plan pays the Epsilon Group, an integrated delivery system (IDS), a capitated amount to provide substantially all of the inpatient and outpatient services that Antler offers. Under this arrangement, Epsilon accepts much of the risk that utilization rates will be higher than expected. Antler retains responsibility for the plan's marketing, enrollment, premium billing, actuarial, underwriting, and member services functions.

2. The Bengal Health Plan pays an independent physician association (IPA) a capitated amount to provide both primary and specialty care to Bengal's plan members. The payments cover all physician services and associated diagnostic tests and laboratory work. The physicians in the IPA determine as a group how the individual physicians will be paid for their services.

From the following answer choices, select the response that best indicates the form of capitation used by Antler and Bengal.

The Eclipse Health Plan is a not-for-profit health plan that qualifies under the Internal Revenue Code for tax-exempt status. This information indicates that Eclipse

The provider contract that Dr. Zachery Cogan, an internist, has with the Neptune Health Plan calls for Neptune to reimburse him under a typical PCP capitation arrangement. Dr. Cogan serves as the PCP for Evelyn Pfeiffer, a Neptune plan member. After hospitalizing Ms. Pfeiffer and ordering several expensive diagnostic tests to determine her condition, Dr. Cogan referred her to a specialist for further treatment. In this situation, the compensation that Dr. Cogan receives under the PCP capitation arrangement most likely includes Neptune's payment for

If Grace Wilson is eligible for benefits under both the Medicare and Medicaid programs, then

Experience rating methods can be either prospective or retrospective. With regard to these types of experience rating methods, it can correctly be stated that

The following statements are about various reimbursement arrangements that health plans have with hospitals. Select the answer choice containing the correct statement.

The Newfeld Hospital has contracted with the Azalea Health Plan to provide inpatient services to Azalea's enrolled members. The contract calls for Azalea to provide specific stop-loss coverage to Newfeld once Newfeld's treatment costs reach $20,000 per case and for Newfeld to pay 20% of the next $50,000 of expenses for this case. After Newfeld's treatment costs on a case reach $70,000, Azalea reimburses the hospital for all subsequent treatment costs.

One true statement about this specific stop-loss coverage is that

The following statements are about federal laws and regulations which affect health plans that offer products and services to the employer group market. Select the answer choice containing the correct statement.

Provider reimbursement methods that transfer some utilization risk from a health plan to providers affect the health plan's RBC formula. A health plan's use of these reimbursement methods is likely to result in

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 10 Jul 2026