We at Crack4sure are committed to giving students who are preparing for the CIMA BA2 Exam the most current and reliable questions . To help people study, we've made some of our Fundamentals of management accounting exam materials available for free to everyone. You can take the Free BA2 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

Johnson & Smith is a huge corporation with many different departments covering hundreds of activities. They had switched to this new budgeting technique as it seemed as though it would help them allocate their

limited funds better.

It was successful to some extent as each manager was required to look at every cost his department accrued. They would then be responsible for coming up with new ways of performing these activities.

It became obvious that certain managers were unable to handle these paperwork intensive demands and so the company will be reverting back to a system that focuses primarily on cost drivers next year.

What budgeting technique will they be using next year?

LC produces a household detergent in a single process. Information for this process for last month is as follows:

(a) Materials input - 11,000 Litres at £2.00 per litre.

(b) Conversion costs - £23,000

(c) Output during the month - 8,000 litres.

(d) There were 2,000 units of closing work in progress which was complete as to materials and 35% complete as to conversion.

(e) Normal loss for the month was 5% of input and all losses have a scrap value of 50p per litre.

(f) There was no opening work in progress.

What was the value of the abnormal loss/gain during the month (to the nearest £)?

An abnormal loss in a process occurs when:

There are four global principles for management accounting which are intended to support organisations in setting a standard and improving their management accounting systems.

Which one of the following helps management determine whether a certain decision will potentially generate, preserve, or destroy value within the business?

Refer to the exhibit.

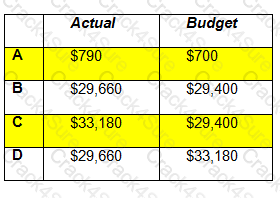

A company budgeted to provide 700 units of service last period for a budgeted variable overhead cost of $29,400. During the period a total of 790 units of service were provided and the variable overhead cost incurred was $29,660.

For effective control of variable overhead cost which two figures should be compared in the budgetary control statement?

Assume that a unit of output is the cost object. Which of the following statements is valid?

Refer to the exhibit.

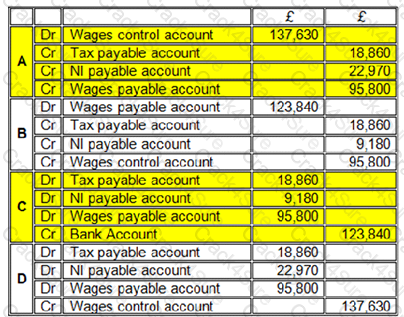

Which of the following journal entries are required to record the wages payable?

The journal entries required to record the wages payable are:

Overhead allocation is best described as:

Which of the following may result in a favourable material price variance? (Select ALL that apply.)

A company operates a full cost system of pricing. Production overheads are absorbed using a pre-determined absorption rate of £3.50 per machine hour. The direct production cost of product A is £15 per unit and it utilises 6 machine hours per unit. The mark-up for non-production costs is 10% of total production cost. The company wants to make a 25% return on sales revenue for all products.

The required selling price for Product A, to two decimal places, is:

Refer to the exhibit.

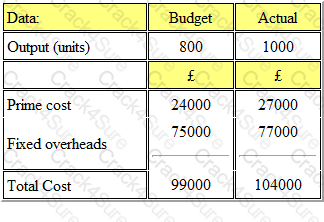

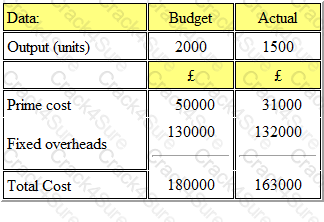

A company issued its production budget based on an anticipated output of 800 units. Actual output was 1000 units. The details of the costs are shown below:

The budget volume variance was:

Refer to the exhibit.

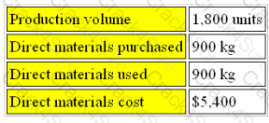

The budget for WP for the month of September contained the following data:

During the month the actual number of units produced was 1,860. The management accounts showed a direct material price variance of $1,200F and direct material usage variance of $180A. The direct materials purchased were 1,200 kg.

The actual quantity of material used in the month was

Refer to the exhibit.

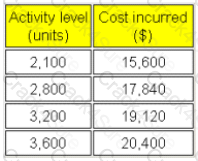

A company has established that a particular cost item is semi-variable. Past records of costs at different levels of activity are as follows:

The fixed cost element for the cost item is:

LC produces a household detergent in a single process. Information for this process for last month is as follows:

(a) Materials input - 11,000 Litres at £2.00 per litre.

(b) Conversion costs - £23,000

(c) Output during the month - 8,000 litres.

(d) There were 2,000 units of closing work in progress which was complete as to materials and 35% complete as to conversion.

(e) Normal loss for the month was 5% of input and all losses have a scrap value of 50p per litre.

(f) There was no opening work in progress.

The value of closing work in progress at the end of the month is closest to:

Which one of the following is NOT a main purpose of management accounting?

Refer to the exhibit.

A company has the following budget information for next year:

The budgeted profit for the year is

Refer to the exhibit.

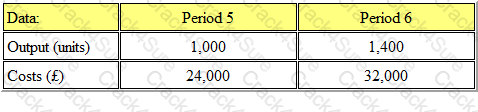

The output and costs for two periods were as follows:

Fixed costs will remain constant, but during Period 7, the variable cost per unit will increase by 25%. The output for Period 7 will be 1,600 units.

The budgeted total cost for period 7 will be:

Which of the following are not relevant costs? Select ALL that apply.

Refer to the exhibit.

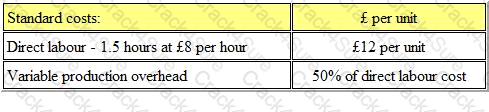

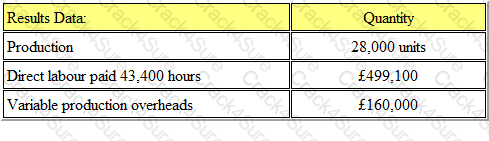

AM Ltd. makes and sells a single product for which the standard cost information is as follows:

Budgeted production for the period is 30,000 units.

The actual results for the period were as follows:

What is the variable overhead efficiency variance?

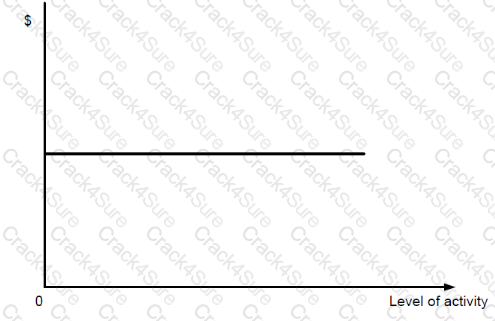

Refer to the exhibit.

Which ONE of the following can be represented by this graph?

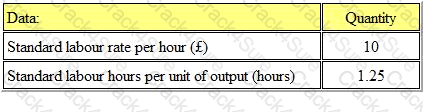

The standard labour hours for all products manufactured by a company include an allowance for idle time. Idle time is budgeted to be 5% of total hours worked. Each unit of product G requires an input of 9.5 active labour hours. The labour rate is $12 per hour.

The standard labour cost shown on the standard cost card for one unit of product G will be

A chemical process has a normal wastage of 8% of input. For the month of June, 5,000 liters of materials were input and there was an abnormal gain of 200 liters.

The quantity of good production achieved was

The gradient of the line plotted on a profit/volume (PV) graph is determined by:

Which of the following is not a relevant cost?

Two rival furniture manufacturers have recently merged together. Before the merge each party had three outlets and one factory each. Now they have two factories, six stores with another 3 planned in the next year.

Previously, one company had operated with function cost centres, looking at costs incurred by each department whilst the other had chosen to look at costs per activity.

Whilst the companies were small this worked and costs were easy to manage and issues could be dealt with quickly and efficiently. Since then costs have gone out of control as the old systems no longer work for this

large, nationwide company.

What is a suitable type of cost centre to use now?

Which of the following would NOT require taking into account the time value of money?

The concept of the time value of money:

A company’s policy is to hold closing inventory each month equal to 10% of the next month’s budgeted sales volume. The budgeted sales volumes of product Q for months 1 and 2 are 1,660 units and 2,300 units respectively.

The production budget for product Q for month 1 is:

A company’s management accountant wishes to calculate the present value of the cost of renting a delivery vehicle. There will be five annual rental payments of $5,000, the first of which is due immediately. The company’s discount rate is 12%.

Which TWO of the following are valid ways to calculate the present value of the rental payments? (Choose two.)

Which TWO of the following are characteristics of Management Accounts? (Choose two.)

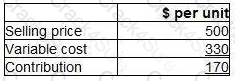

A company which manufactures and sells one product has fixed costs of $80,000 per period. The selling price per unit of $25 generates a contribution/sales ratio of 40%.

How many units would need to be sold in a period to earn a profit of $10,000?

A company is appraising two projects. Both projects are for five years. Details of the two projects are as follows.

Based on the above information, which of the following statements is correct?

Refer to the exhibit.

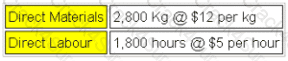

T operates a process costing system. Data is available for Process A for the month of July.

Inputs for the month:

Normal losses are 15% of input and can be sold for $6 per kg. Actual output was 2,600 kg. There is no opening or closing work in progress for the period.

What is the value of the output from the process in the month?

Refer to the exhibit.

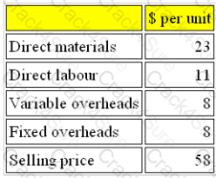

SL manufactures a single product, the cost and selling price of which are given below:

Fixed overheads per unit are based on a budgeted production volume of 25,000 units.

Budgeted sales are assumed to be 25,000 units.

If all costs increase by 5% but selling price remains the same, by how much must sales change from the budgeted volume to achieve the same budgeted profit?

The variable overhead expenditure variance is:

Each unit of product GM requires 4 labour hours to be produced. 25% of the units will be completed during overtime hours.

Sales of 24,000 units are planned and finished goods inventory is budgeted to rise by 2,000 units.

If the wage rate is £6 per hour and the overtime premium is 50%, what is the budgeted labour cost?

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

The sales volume contribution variance for the period was:

In a company that manufactures many different products on the same production line, which TWO of the following would NOT be classified as indirect production costs? (Choose two.)

Which of the following cannot be used to split costs into fixed and variable elements?

Refer to the exhibit.

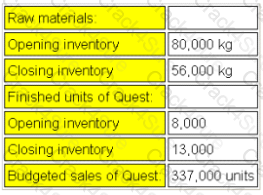

Data for October's budget for product Quest for the month of October are given below:

Each unit of Quest requires 6kg of raw materials. Strict quality control procedures are applied to the manufacturing process and normal rejection levels are 5% of finished units.

The raw materials purchases budget for the month of October is:

An overtime premium may be defined as:

A company uses full cost pricing. The unit costs for product Z are given below.

What price per unit should be charged in order to achieve a profit margin of 20%?

Give your answer to the nearest cent.

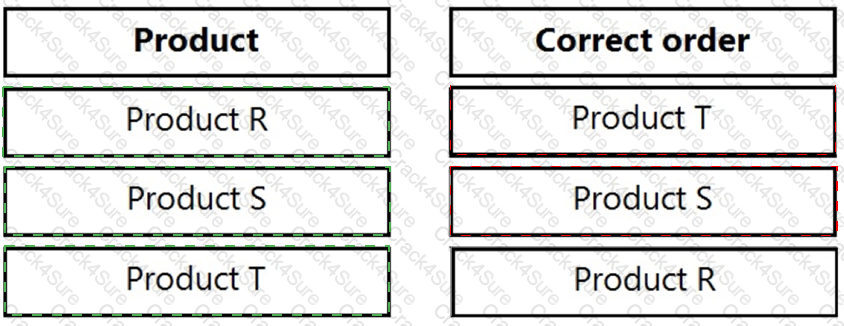

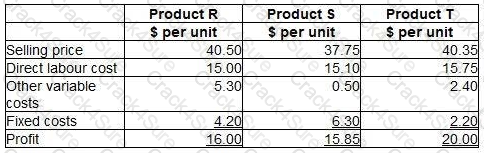

A company manufactures three products using the same direct labour which will be in short supply next month. No inventories are held. Data for the three products are as follows:

The fixed costs are all committed costs and cannot now be altered for the next month.

Place the labels against the correct product to indicate the order of priority for manufacture that will maximise the profit for the next month.

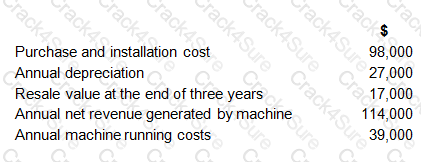

A company is considering investing $57,000 in a machine that will last for five years, after which time it will have no value. The machine will generate additional revenue of $190,000 each year. Annual running costs, including depreciation of $11,400 will amount to $168,400.

Assuming that all cash flows occur evenly, the payback period of the investment in the machine is closest to:

Refer to the exhibit.

A company issued its production budget based on an anticipated output of 2000 units. The actual output for the period was 1500 units. The details of the costs are shown below:

What was the budget expenditure variance?

Which of the following would have an impact on the cash budget?

(a) Change in payables terms

(b) Change in the rate of depreciation

(c) Change in the percentage discount allowed

(d) Change of inventory holding policy

The wages of a machine operator who is paid by the hour would be described as A.

In which industries would idle time not be expected? (Select ALL that apply.)

A company uses an integrated accounting system.

The accounting entries for the issue of direct materials to production would be:

Refer to the exhibit.

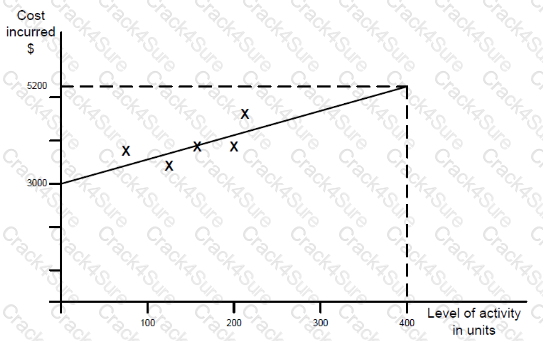

The following scattergraph has been drawn for a certain cost in recent periods.

Based on this scattergraph the variable cost per unit is:

A feature of a normal curve is that it is asymptotic, meaning that _______.

Refer to the exhibit.

The following standard cost information relates to the production department of BE Ltd.

The actual data for the month of March was as follows:

What is the direct labour efficiency variance (to the nearest whole number)?

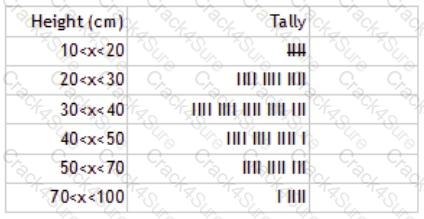

A tomato producer is investigating the correlation between the height of his plants and the size of the tomatoes. He has tallied up his height results and produced this table.

Using the information provided, find the median and modal class and correctly select these answers from the list.

Median = 30 Modal class = 30 Median = 40 Modal class = 40>x>50

It is company policy that the closing inventory of finished goods must be equal to 10% of the following month's budgeted sales. The budget sales for November and December are 50,000 and 40,000 units respectively.

The budgeted production for November will be

A cash budget is an example of a:

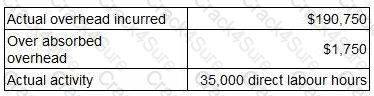

Over absorption of overhead will always arise when:

Which THREE of the following statements could explain why an adverse material price variance has arisen?

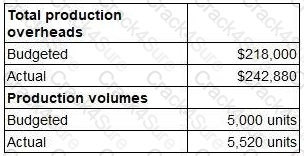

FL uses an absorption costing system. The overhead absorption rate for production overheads is $8.60 per direct labour hour.

Budgeted production overhead costs for the year were $473,000 and actual costs incurred were $468,000. 56,000 labour hours were used.

Which ONE of the following statements is correct?

PQR Manufacturing Ltd. has £3,000,000 of fixed costs for the forthcoming period. The company produces a single product 'X', which has a selling price of £75 per unit and total cost of £50.

75% of the total cost represents variable costs.

What are the break-even units?

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours. In the period actual labour hours were 10,600, 400 hours below budget. Actual overheads for the period were £234,680 and there was an under-absorption of overheads of £1,480.

What was the budgeted level of overheads?

In a company's sales ledger department, one additional invoice clerk is needed for every eighty customers added to the customer database. The total salary cost of invoice clerks is best described as:

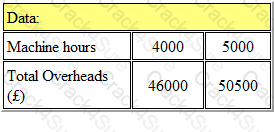

Refer to the Exhibit.

PJ Ltd has forecast that the relationship between total overheads and machine hours will be as follows:

If the budget is to be based on 4,000 machine hours, the variable overhead absorption rate will be:

*per machine hour.

Give your answer to 2 decimal places.

Refer to the Exhibit.

The following budgetary information is available for a department in a manufacturing company:

The production overhead absorption rate percentage, when the percentage on prime cost is used, is:

The management accountant has completed the appraisal of an investment in new office equipment.

It has now been discovered that the cost of capital used in the appraisal should have been higher.

What will be the effect on the calculated net present value (NPV) and the payback period?

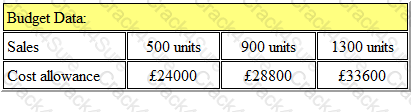

Refer to the exhibit.

Budget information for 'Crome Ltd' is as follows:

The budgeted cost allowance for the sale of 1000 units would be:

The wages of a machine operator who is paid a guaranteed minimum wage plus a bonus for each unit produced would be described as A.

Apex Plc has budgeted to sell 8,000 units of A in the year. Opening inventory of A is estimated at 1,000 units and the company plans to reduce inventory levels of all products by 15%.

What will be the production budget (in units) for the year?

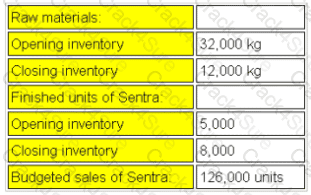

Refer to the exhibit.

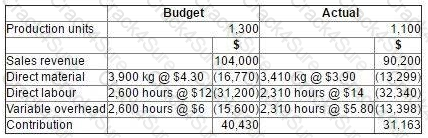

The budget for product Sentra for the month of August is given below:

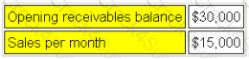

Refer to the Exhibit.

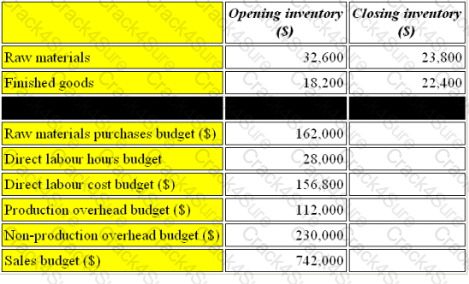

CM has produced the following budget information for next year:

The opening receivables balance represents 2 months sales. It is expected that the same level of sales will continue at an even rate throughout the year.

In an effort to improve receivables collection periods it is proposed to offer a discount of 5% for payment by cash. It is expected that 20% of customers will pay by cash. Of the remaining 80% credit sales, 40% will be settled within 1 month and 60% are expected to settle within 2 months.

What are the budgeted cash receipts from cash and credit sales in the year?

The net present value (NPV) of an investment is as follows.

NPV at 14% = $6,320

NPV at 18% = ($4,600) negative

The internal rate of return (IRR) of the investment is closest to

Prime cost is:

Refer to the Exhibit.

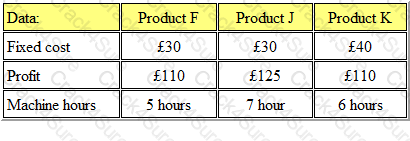

Zepher Ltd. manufactures three products, which require the same type of machine. The following fixed cost and profit per unit is available:

In a period in which machine hours are in short supply, which of the following options is the rank order of production?

Answer is:

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours.

Actual labour hours were 10% below budget for the period and overheads incurred were 10% above budget for the period. This would result in:

In investment appraisal, the internal rate of return is

Which of the following is the LEAST appropriate basis on which to apportion the insurance costs of plant and machinery:

Fixed costs can best be described as:

An increase in the variable cost per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

Which of the following statements is correct?

i. sector bodies use budgetary planning and control systems

ii. costing cannot be used by public sector bodies because they have no measurable output

iii. in public sector bodies tend to focus on cost management therefore they have no need for non-financial information

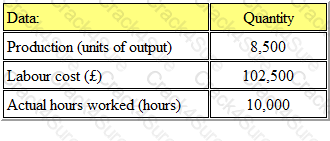

Refer to the exhibit.

A company is considering purchasing a machine that will have a useful life of three years after which time it will be sold. Relevant cash flows relating to the purchase and operation of the machine are as follows.

The annual cost of capital is 14%.

The net present value of the investment in the machine is, to the nearest whole $:

The materials price variance will be adverse when:

In an integrated cost and financial accounting system, the accounting entries for the cost of production units completed in the period would be:

Refer to the exhibit.

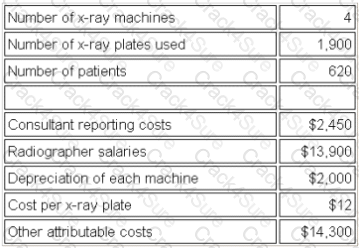

The following data are available for last period for the x-ray department of a local hospital:

The x-ray department cost per patient for last period was (to the nearest $0.01) is:

C Ltd produces a chemical in a single process. Information for this process last month is as follows:

(a) Opening work in progress - 10000 kg valued at £10000 for direct material and £7500 for conversion costs.

(b) Materials input - 25000 kg at £1.10 per kg.

(c) Conversion costs - £17000

(d) Output during the month - 23000 kg.

(e) There were 7500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(f) Normal loss for the month was 10% of input and all losses have a scrap value of 80p per kg.

What was the value of normal loss during the month?

An increase in the selling price per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

Refer to the Exhibit.

PD manufactures a product in a process operation. Normal loss is 5% of input and occurs at the end of the process. The following data is available for the month of August:

Scrapped units have no value.

There was no opening or closing work in progress for August.

What is the value of the abnormal gain in August?

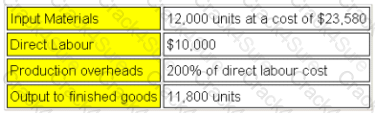

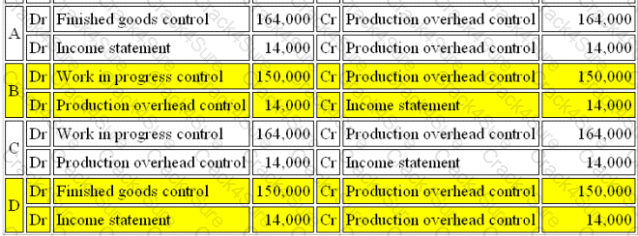

Refer to the exhibit.

WS operates an integrated accounting system. Transactions relating to production overheads for the month of May were as follows:

Indirect Material costs were $15,000

Indirect Labour Costs were $45,000

Production overheads of $58,000 were incurred during the period.

Depreciation of factory machinery amounted to $32,000.

Overheads costs absorbed by production using a standard absorption rate was $164,000 for the period.

What are the correct entries to record the absorption of production overheads for the period?

The correct set of entries to record the absorption of production overheads for the period is:

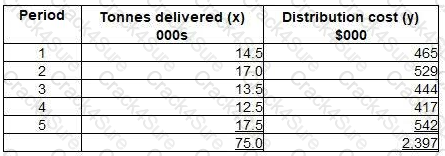

The following data are available for a delivery company. The table shows the number of tonnes delivered (x) and the associated distribution cist (y) in recent periods.

Further analysis of this data has determined the following:

?xy = 36,427?x2 = 1,144

Using least squares regression analysis, calculate the variable cost per tonne delivered. Give your answer to the nearest cent.

Which of the following is NOT a valid purpose of budgeting?

Which THREE of the following are included in the Global Management Accounting Principles? (Choose three.)

A company has two production departments and two service departments (Maintenance and Stores). The overhead costs of each of the departments are as follows.

The following equations represent the reapportionment of each of the service department overheads to the other.

M = 4,700 + 0.1S

S = 5,800 + 0.2M

Where M = total Maintenance overhead after reapportionment from Stores

S = total Stores overhead after reapportionment from Maintenance

60% of the total Maintenance overhead and 50% of the total Stores overhead are to be apportioned to Production Department 1.

The total production overhead for Production Department 1 after reapportionment of the service departments’ overhead costs is closest to:

The staffing policy for a supermarket is to have one cashier station open for every forecasted 20 customers per hour. Cashiers are hired by the hour as and when required, and do not perform any other duties.

The cost of the cashiers in relation to the number of customers would be classified as which type of cost?

A company has spent $5,000 on a report into the viability of using a subcontractor. The report highlighted the following:

A machine purchased six years ago for $30,000 would become surplus to requirements. It has a written-down value of $10,000 but would be resold for $12,000.

A machine operator would be made redundant and would receive a redundancy payment of $40,000.

The administration of the subcontractor arrangement would cost the company $25,000 each year.

Which THREE of the following are relevant for the decision? (Choose three.)

The International Federation of Accountants (IFAC) stated that it was important that “accountants in business” should understand what the drivers of stakeholder value are. Which of the following statements is valid?

A company absorbs production overhead using a direct labour hour rate. Data for the latest period are as follows:

What is the overhead absorption rate per direct labour hour? Give your answer to one decimal place.

A confectionery manufacturer is considering adding a new product to the current range. Forecast data for the product are as follows.

Incremental fixed costs attributable to the new product are forecast to be $24,000 each period.

The forecast sales volume of 180 units is insufficient to achieve the target profit of $10,000 each period.

Which of the following statements is correct?

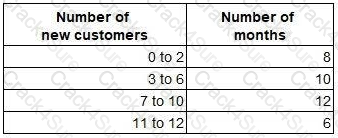

Every month for the last three years, a company has recorded the number of new customers for that month. The data have been summarised and grouped as follows:

What is the arithmetic mean of the number of new customers per month?

A company makes and sells a range of products. The standard details per unit for one of these products, product X, are as follows.

To meet sales demand, the company must obtain 2,000 units of product X next month. There is sufficient labour capacity to produce 1,500 of these units in-house during normal time. However, any production above this level would require overtime working which would be paid at a premium of 50%.

The company can buy as many units of product X as it wishes next month from an external supplier at a price of $120 per unit.

What is the total financial benefit to the company of purchasing the appropriate number of units from the external supplier rather than producing them in-house?

The following is an extract from a budgetary control report for the latest period:

The budget variance for prime cost is:

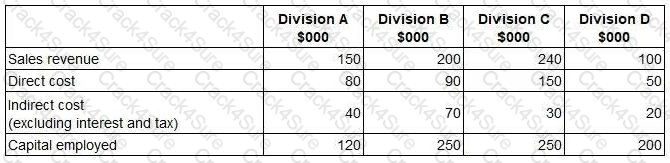

An organisation’s management report contains the following data:

Which division has the highest operating margin percentage?

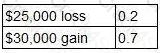

A project is about to be launched. Two of the three possible outcomes and their associated probabilities are as follows:

The remaining possible outcome is a $70,000 gain.

What is the correct calculation of the expected value of the project?

Which of the following is NOT a characteristic of useful operational level information?

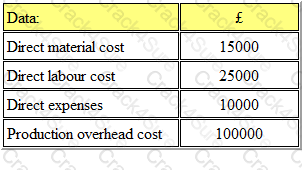

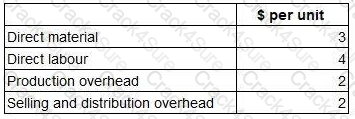

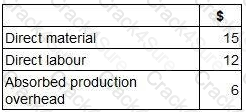

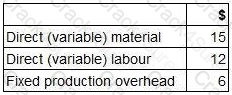

A company produces a single product for which the following cost data are available.

Analysis by the management accountant has shown that 100% of direct material cost and 50% of direct labour cost are variable costs. 50% of production overhead and 100% of selling and distribution overhead are variable costs.

What is the marginal cost per unit?

Data for the latest period for a company which makes and sells a single product are as follows:

There were no budgeted or actual changes in inventories during the period.

The variable overhead expenditure variance for the period was:

Which of the following statements regarding variances is valid?

A new product requires an investment of $200,000 in machinery and working capital. The total sales volume over the product’s life will be 5,000 units. The forecast costs per unit throughout the product’s life are as follows:

The product is required to earn a return on investment of 35%.

What unit selling price needs to be achieved?

In order for the information in a management accounting report to be authoritative its contents must be:

In responsibility accounting, costs and revenues are grouped according to:

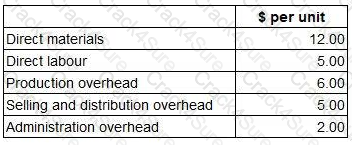

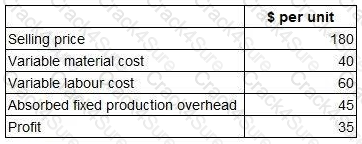

The forecast costs per unit for a new product are as follows:

The company uses marginal cost plus pricing and all products are required to achieve a 40% margin.

What would be the selling price per unit?

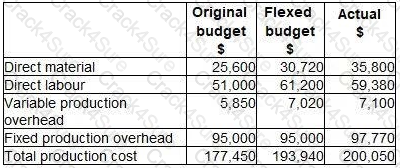

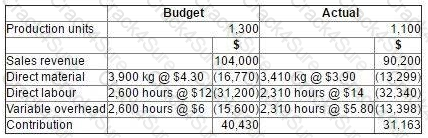

The following data relate to the latest period.

A statement is to be prepared that reconciles the difference between the flexible budget profit and the actual profit.

Which TWO of the following will appear on this statement? (Choose two.)

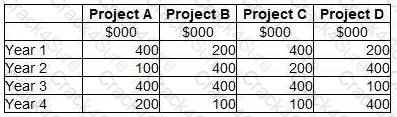

A management accountant has forecast the following cash inflows from four potential projects.

All four projects require the same initial investment and will last for four years. They all result in a positive net present value but only one of the projects can be undertaken.

Which project should be selected?

The following data are available for a company that produces and sells a single product.

The company’s opening finished goods inventory was 2,500 units.

The fixed overhead absorption rate is $8.00 per unit.

The profit calculated using marginal costing is $16,000.

The profit calculated using absorption costing and valuing its inventory at standard cost is $22,400.

The company’s closing finished goods inventory is:

A company uses an integrated accounting system. The following data relate to the latest period.

At the end of the period, the entry in the production overhead control account in respect of under or over absorbed overheads will be:

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 10 Jul 2026