We at Crack4sure are committed to giving students who are preparing for the CSI AFP-Exam-1 Exam the most current and reliable questions . To help people study, we've made some of our Applied Financial Planning Certification Exam 1 (AFP) exam materials available for free to everyone. You can take the Free AFP-Exam-1 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

Jimi and Macy, both age 26, consider themselves risk averse. After reviewing their budget with their financial planner, they discovered that they have a negative cash flow every couple of months due to their discretionary spending habits. What would be an appropriate strategy for their financial planner to recommend to the couple to manage their negative cash flow?

Which assets will flow through an estate?

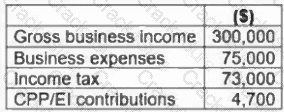

Jackson, a wealth advisor, is helping Terry, a self-employed IT professional, determine his net income. The goal is to develop a budget and savings strategy for the year ahead Terry has provided the information below:

What is Terry’s net business income?

Richard pays periodic spousal support and child support under a written separation agreement. Which statement is generally correct?

Lois is reviewing her client Raj's retirement plan. To stay on track, Raj's TFSA (with a current balance of $10,000) will need to be worth $42,000 in five years. Raj is able to contribute his annual bonus of $5,000 at the end of each year. For Raj to stay on plan, what rate of return does Lois need to be targeting?

The Andersons, a young couple, meet with their financial planner to review estate-planning opportunities. They recently had a third child and are looking for the most cost-effective strategy to put in place during their working years to increase their estate value and reduce the tax burden at death for the benefit of their children. What should the financial planner recommend?

Bruna is a senior financial planner. At 4 p.m. on Friday afternoon (an hour before closing), her manager asks her to complete the following:

Fix a mutual fund trade that was entered incorrectly by a junior financial planner.

Call her client to advise him that his account is overdrawn, and the bank will refuse recent payments unless he credits the account before 5 p.m.

Bruna determines she can only complete one of the two tasks before the end of the business day. How should Bruna address her supervisor's request?

Dianna is visiting with Karen, her Financial Planner, and is excited to report that she has just bought her dream home. She has also let Karen know she Is meeting with an insurance representative to purchase a whole life insurance to cover her 20-year mortgage. Why might Karen suggest Dianna consider term life insurance instead?

Carla, a financial planner, is meeting with a long-standing client, Jonathan. Jonathan informs Carla that he is upset and disappointed with the negative returns experienced with his investment portfolio. After acknowledging Jonathan's concerns, what should Carla's first step be in addressing his complaint?

A business owner completes an estate freeze, taking back preferred shares with a fixed redemption value while children receive common shares. What is a primary risk of this strategy for the owner?

In 2019, Glenda, age 46, visited her financial planner to discuss her goal of retiring at the age of 65. Glenda had questions about whether she qualified for the maximum amount of CPP and OAS benefits as she had immigrated to Canada just 10 years earlier to take a job as a nuclear technician. What should her financial planner have told her?

Sarah Jones is an incorporated owner of a successful manufacturing company. She currently has a large month to month cash flow surplus. This is expected to continue until she retires in seven years. Her personal mortgage is up for renewal. She needs to borrow $50,000 so that she can replace a piece of equipment that is needed in the manufacturing process. She would like a solution that results in paying the lowest interest cost over the life of the loan. Which loan product should the financial planner recommend to Sarah? Assume monthly compounding for all products and no pre-payment options.

Bill is reviewing his credit bureau after being declined for a loan. He believes a loan that does not belong to him is appearing on the report. Which section should he review most closely?

Kendrick, age 55, owns a successful small business, ZXC Inc., valued at $800,000. Kendrick has extensive savings outside of the business and would like to pass the company onto his son at some point in the future. Kendrick expects the business to increase in value $25,000 per year. If Kendrick decides to use an estate freeze to reduce the amount of taxes he will be required to pay, his financial planner should recommend that he implement the estate freeze at which point in relation to gifting the business to his son?

Sheeba is a financial planner and meeting with Ivana, a new client. She explains that part of her process is to recommend products and services, but prior to doing so, she will closely investigate the options to ensure they match up with Ivana's goals. Which professional responsibility has Sheeba demonstrated to Ivana?

Samantha is meeting with a financial planner for the first time, seeking help with both investing and debt management. She's finding it hard to get ahead because she recently graduated with student debt, started a new career in her field, and is adding credit card debt each month. What recommendation should the financial planner propose?

A client, age 60, is in a low tax bracket today and expects a larger taxable pension after age 65. She has TFSA and RRSP room. Which contribution priority is generally more appropriate?

A client completed a financial plan two years ago. Since then, she has divorced, changed jobs, and purchased a new home. What is the planner’s most appropriate recommendation?

Richard reviewed his divorce settlement from his partner Alex with his advisor Maria. He is deciding between providing a lump sum spousal support payment of $60,000 or making monthly payments. If Richard’s income is $200,000 and Alex’s income is $40,000, what should Maria advise Richard about the tax implications for both Richard and Alex in regard to the lump sum payment?

How should Jenny, a financial planner, explain the benefits of a fee for service method of compensation to a prospective client?

Ronny, a successful business owner, established a discretionary family trust earlier this year as a means to split income with his children. Ronny's children are both under the age of five and are both income and capital beneficiaries of the trust. He is concerned that the 21-year rule will result in a significant amount of tax resulting from unrealized capital gains. What strategy would be best if Ronny's goal is to minimize the total amount of tax payable by the trust and/or beneficiaries at the 21-year mark?

A planner establishes a long-term target portfolio of 65% equities and 35% fixed income based on the client’s objectives and constraints, with periodic rebalancing. Which allocation approach is being used?

Rob, age 42, is married with three children in elementary school. He works as an operations supervisor at a small manufacturing company, earning $70,000 annually. Rob asks his financial planner, Wendy, to liquidate his GIC investments worth $55,000 in order to use the sale proceeds to purchase a gold stock referred to him by his friend who expects the stock to appreciate significantly. Rob has not purchased stock before. What should be Wendy's reaction to Rob's query?

A client sends an email alleging that a mutual fund recommendation was unsuitable because the fund declined sharply after purchase. The client asks for compensation. What is the financial planner’s first professional obligation?

Jonathan owns a medium size consulting firm and earns an average annual income of $150,000. He is reviewing his retirement plan with his financial planner. Jonathan asked his planner about retirement compensation arrangement and how this may benefit him. What should his financial planner tell him?

A client borrows $100,000 to invest in a non-registered portfolio expected to generate interest and dividend income. What tax principle is most relevant?

John and Jerry's financial planner have recommended they review their budget. What is the primary purpose of the budget?

Edward is risk averse and has limited investment knowledge. He will only purchase 100% guaranteed products insured by the CDIC. Edward is meeting with his financial planner, Marissa, for the third time this year about rates, and starts the meeting by criticizing her employer for paying such low returns on GICs. Edward says he is considering taking his business elsewhere. How should Marissa respond to Edward’s comments?

William and Jennifer are selling their business which qualifies as a Canadian-controlled private corporation. When the sale is complete at the end of this year, William and Jennifer will each receive $4 million for their common shares which have nominal cost. Jennifer has unused capital losses from previous years. They are meeting with Laurel, their financial planner, to discuss the tax implications of the sale. Based on the information provided, what should Laurel recommend to William and Jennifer so that they are best able to make use of the Lifetime Capital Gains Exemption?

A couple has stable employment, two dependants, and essential monthly expenses of $5,200. They have no emergency reserve. Which recommendation is most appropriate before increasing long-term investment contributions?

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 05 Aug 2026