We at Crack4sure are committed to giving students who are preparing for the IFSE Institute LLQP Exam the most current and reliable questions . To help people study, we've made some of our Life License Qualification Program (LLQP) exam materials available for free to everyone. You can take the Free LLQP Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

Gino, an insurance of persons representative, is cleaning his office and going through old files. He comes across a file from a former client, Nathan, who owned a 20-year term insurance policy that was cancelled 3 years ago. Nathan now has a different representative and Gino no longer has any contact with him. Gino would like to know if he can destroy Nathan's file.

Which of the following options is CORRECT?

Coraline owns a $250,000 whole life insurance policy. She purchased the policy last year and does not have any funds accumulated in her cash surrender value (CSV). On December 30, Coraline assigns the policy to the cancer foundation, and she plans on continuing to pay the $200 monthly premium. Coraline calls her accountant James to ask him how much of her donation she will be able to use to obtain a charitable tax credit this year.

Zaid married Baheya five years ago in Montreal. A year later, Zaid purchased two individual term-life insurance policies, one on his life and the second on Baheya’s life, each with a death benefit of $250,000. The marriage didn't last long, and the couple divorced shortly thereafter. Baheya went on to marry Omar, and the new couple had a baby together, named Darwish.

Last week, Baheya died in a car accident. While settling her estate, Omar discovered that no beneficiary was designated on Baheya’s life insurance policy.

To whom will Baheya’s death benefit be paid?

Rene and Christine are 42-year-old twins. They are currently in the middle of a career change and have decided to become entrepreneurs by buying a food franchise.

They are both in excellent health and only Rene is an average smoker.

In setting up the financial structure of their business, they each decided to take out a $400,000 10-year term life insurance policy, designating each other as irrevocable beneficiary.

What can we say about the premiums for the life insurance policies that will be issued?

Jean, who is in business, would like to understand why his segregated funds, which resemble mutual funds, allow this type of asset to be sheltered from creditors. How should Patrice, his financial security advisor, answer?

Jasper owns TeleVida, a successful production company with over 50 employees. He wants to expand the company by opening an office in another province. Jasper needs to take out a $500,000 20-year loan to make this expansion happen. However, he wants to make sure that if he dies while there’s an outstanding balance on the loan, the balance will be paid in full by the insurance company.

Alexandre has just become a father. He wishes to take out a life insurance policy from Antoine, an insurance of persons representative. During their meeting, Alexandre mentions his love of mountain climbing. What should Antoine do?

Last month, Suzanne purchased a life insurance policy from a local agent. The agent told her that the policy would accrue a cash value that she could draw from in her retirement years and that the premium would never increase. After recently meeting with a close friend, who is a retired insurance advisor, she was dismayed to learn that what was sold to her is in fact a term policy with no cash value. If Suzanne wishes to make a formal complaint against the agent, which authority can assist her in doing so?

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

Brian gives his lawyer Dave $200,000 that will be used as a down payment to purchase a condo. Brian received these funds from his mother’s life insurance death benefit. The money is deposited into Dave’s trust account. Unbeknownst to Brian, Dave is going through financial hardship. If Dave files for bankruptcy while Brian's funds are still in his trust account, can the bankruptcy trustee seize the funds?

Bea is a married 65-year-old woman applying for a life insurance policy. She meets with Stanley, her insurance agent, to review her insurance needs. Stanley inquires if Bea has started receiving Old Age Security (OAS) and Canada Pension Plan (CPP) benefits. Why is it important for Stanley to know this?

Goran and Tanja married two years ago. Last year, they purchased and moved into a three-bedroom house in the suburbs. The current balance on their mortgage is $655,000. They meet with Ljubomir, an insurance agent, to purchase a joint term life insurance policy to cover the mortgage. When Ljubomir asks about their existing coverage, Goran shares that he has none. Tanja explains that she owns a universal life (UL) policy with a level death benefit of $50,000 and a cash surrender value (CSV) of $5,000, purchased 6 years ago from another agent. Tanja would like to surrender her UL policy and use the $5,000 CSV to pay for a trip to Europe. What additional information about Tanja's UL policy does Ljubomir need to collect?

Josh is an established advisor who specializes in group benefits. He recently hired Bryan as a marketing manager. Bryan will be responsible for advertising and creating a social media platform for Josh's company. Among other things, Bryan is developing a monthly electronic newsletter, which he plans to email to potential and existing clients. However, because this is a brand new initiative, none of the would-be recipients has subscribed to the newsletter or asked to receive any such communication from Josh's company. What law should Josh and Bryan be mindful of before sending their newsletter?

Agatha and Peter run a successful sole proprietorship. They are 68 and 70 respectively. Peter has a huge registered investment portfolio that will result in significant tax consequences upon his death. When both of them have passed away they would like their registered investment portfolio to go to their son, Alexander, who is 48 years old. The family would like to purchase life insurance to offset the tax liability.

Which of the following plans would best suit the family?

Maeve is an Ontario resident. Fifteen years ago, she purchased a $250,000 whole life insurance policy and named her husband Guillaume as the primary beneficiary and her 4-year-old son Edwin as the contingent beneficiary. Last week, Tasha, Maeve's insurance agent called her to ask if she has had any life changes that would warrant a meeting to review her insurance coverage. Maeve informs her that over the last year she divorced Guillaume and that she is now living with her new boyfriend Eduardo. Tasha asks to meet Maeve to review her beneficiary designation. Who will receive Maeve's death benefit if she dies today?

Germain is a life insurance agent. This morning, he receives a call from Jason, whose wife, Rosalie owned a $50,000 life insurance policy that she purchased from Germain seven years ago. Jason explains that Rosalie had a heart attack and died last week. Germain promises to help as much as he can.

Donald is married and has two children, ages 3 and 5, one of whom is severely disabled and will never be able to live independently. He is considering buying $500,000 of life insurance to guarantee care for his disabled child for his lifetime. He also wishes to insure his 20-year mortgage of $250,000 to ensure that his family can remain in their home in the event of his death.

What life insurance policy would you recommend to Donald?

Jeremy, aged 35 and Emily, aged 40, are common law spouses and have 3 children, Jack, Maddie, and Grace. They are reviewing their life insurance coverage with Mark, a local life insurance agent, to ensure they have adequate coverage. Currently, Jeremy and Emily both have term life insurance in the amount of $200,000. Jeremy recently inherited a family cottage valued at $400,000 (ACB of $200,000), which him and Emily hope to pass on to their children one day. Mark informs Jeremy & Emily of the potential tax liability of passing the cottage to their children and advises them that they should consider purchasing additional life insurance.

How much life insurance should they purchase to cover the future tax liability of the children taking into account a tax rate of 50%?

Abishola purchases segregated funds from her insurance agent Bob. Before finalizing the transaction, she tells Bob that she will need the funds in a few months to make a down payment on a condo. Later, when Abishola calls to withdraw her funds, Bob informs her that she will incur a fee for withdrawing her funds prematurely. Abishola complains to Bob, and then to Bob's supervisor, without receiving a satisfactory response. To which organization can Abishola escalate her complaint?

Johann owns a $250,000 whole life insurance policy. The policy has a cash surrender value (CSV) of $55,000 and an adjusted cost basis (ACB) of $30,000. Johann would like to cancel his policy and use the cash surrender value to fund a new business. If his marginal tax rate is 40%, how much will he have left after cancelling his policy?

Francis owns a $250,000 insurance policy with an accidental death and dismemberment (AD&D) rider. Francis calls his insurance agent Andrew to inform him that he permanently lost the use of his right hand. He explains to Andrew that his brother shot him when he broke into his brother’s house to recover a gold watch that was rightfully his. Francis wants to know how much he will receive from his AD&D rider.

Dale meets with his last appointment of a busy workday. He is helping his client Larry fill out a disability insurance claim form. Larry suffered a heart attack a week ago and is at home recuperating. Larry will be unable to work for the next 6 months and needs the benefits as soon as possible to cover his expenses. The at-home appointment takes a little longer than scheduled and Dale finds himself rushing to his son’s big hockey tournament. In his haste, he puts Larry’s form in his briefcase and subsequently forgets to submit the form. Which responsibility did Dale breach?

Natalie and Ted, who are both 40, meet with an insurance agent to discuss their life insurance needs. They have four major concerns. Their first concern is that Natalie is the primary income earner: if something happened to her, Ted would not be able to provide their two young children with the life they are accustomed to. Their second concern is that if something were to happen to Ted, Natalie would have to pay for childcare. The third issue is that they want to make sure the mortgage on their primary residence is paid off in the event something happened to either of them. Lastly, Natalie is concerned about the tax liability on the family cottage when it gets passed on to the kids. The family cottage is fully paid. The agent notes that most of the couple's concerns could be addressed with term life insurance products.

Which of their concerns can only be addressed with a permanent life insurance product?

Laraine wants to purchase an Individual Variable Insurance Contract (IVIC) because of the death benefit guarantee as she has been ill. She has decided on a segregated fund which has, as its underlying asset, units of a mutual fund that invests in North American common shares. Her insurance agent, Jeffrey, wants her to understand key issues before she completes and signs the application. What should Jeffrey do?

Three years ago, Douglas purchased a whole life insurance policy with numerous supplementary benefits and riders. Today, he meets with his doctor who informs him that he has late-stage colon cancer and has only a few months to live. Even with surgery, his chances of survival are low. Douglas calls his insurance agent, Penny, to ask her what he should do to obtain a benefit immediately.

Ae-Cha starts working for the manufacturer, Premier Vibe Inc., a company that offers its employees group insurance with Sprout Life Insurance. Ae-Cha meets with Devon, the group insurance representative, and learns that her group plan includes $75,000 of life insurance coverage. Ae-Cha would like to know who designates the beneficiary on the life insurance.

Six years ago, Gerard, aged 28, purchased a life insurance policy.

Gerard just got married to Tanya, and they both want to purchase more insurance. Reviewing Gerard’s policy, Tanya notices that Gerard neglected to mention that he had migraines due to concussions suffered from playing football when he was a teenager. Gerard did not intentionally neglect to mention the migraines as the migraines were never an ongoing issue once he stopped playing football.

Which statement is true?

Cecilia, a licensed life insurance agent, delivers a life insurance policy to her client Tony, a newly landed immigrant. Tony would like to pay the policy using the pre-authorized monthly payment method. However, he does not have a bank account in Canada yet and doubts he could find the time to open one in the next few days. Cecilia offers to open a savings account for him, but Tony is unsure whether she is licensed to do that. What should Cecilia tell Tony to reassure him that she can open a savings account on his behalf?

Paola, an employee at Horizon Pharmaceuticals, was recently diagnosed with depression. She is unable to work and is receiving tax-free disability insurance benefits due to her condition. Paola is deeply indebted, and her creditors have been garnishing a portion of her pay for the last year. She is worried about her creditors also garnishing her disability benefit.

Can her disability benefits be seized by her creditors?

Mike and Todd are both agents with Superior Insurance Company. Every Friday, they have lunch together at the local pub. One Friday, Mike forgets his wallet, so Todd pays both bills. Mike has a sales appointment that afternoon, where he will be signing a small term life insurance policy on a child. He decides to simply indicate that Todd is the agent of record so that Todd gets the compensation for the sale—an easy way to pay him back for lunch! What practice is Mike engaging in?

Bernadette, a 27-year-old single woman, earns $78,000 annually as a production assistant. She meets with Howard, her insurance agent, to purchase an accidental death and dismemberment insurance contract. Bernadette fills out the application form, the application is accepted, and the effective date is the date of acceptance of the application. Why is the effective date of Bernadette’s policy the same as the date of acceptance?

It’s Friday afternoon and Olivier, an insurance agent, has just received the paper copy of his client’s insurance contract. Olivier is about to leave on a three-day weekend, and he's already late for his camping reservation. He wonders if he should delay his departure to deliver the document, or if it can wait until he gets back on Tuesday. How long does Olivier have to deliver the contract?

Kaamil meets with Omar, his insurance agent, to purchase a whole life insurance policy. Kaamil wants to name his wife Ofra as the irrevocable beneficiary of the policy. Before proceeding, which of the following considerations should Omar CORRECTLY ask his client to reflect on?

Insurance of persons representative Véronique is meeting clients referred by an acquaintance for the first time. Observing some suspicious behaviours on their part, Véronique is thinking about reporting the transaction to the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC). Which behaviours are signs of suspicious transactions?

Miguel applied for a disability insurance policy nearly three months ago. He recently received notice from his agent that his application was approved, with an exclusion applicable to his lower back due to a prior injury. The agent brought the exclusion amendment with the policy at the delivery appointment. Miguel signed and accepted it. He gave the agent a copy of a void cheque to set up direct billing for the premiums, but asked that they wait three days to draw the first premium, to coincide with his payday. The insurer drew the premium three days later, as requested. When did Miguel's policy take effect?

Benjamin is a financial security advisor working for the Larson Group. He is following a mandatory compliance training session given by Andrew, the compliance manager. Andrew explains the importance of following the Chambre de la sécurité financière code of ethics, and Benjamin would like to know to whom the code of ethics applies.

What is Andrew's CORRECT response?

Edward and Shirley initiated a whole life insurance application for their daughter Christine when she was 15 years of age. As Christine was a student with limited income at the time, the agent set Edward and Shirley jointly as owning and paying the premiums of this policy. Edward was designated beneficiary. Who is the policyholder?

After meeting with his advisor Monica, Tom agrees to apply for a $50,000 whole life insurance policy. Monica tells him that the monthly premium will be $40 per month. Monica is advised by underwriting that Tom qualifies for an additional $10,000 critical illness rider, and that the new premium would be $50 per month. Monica advises underwriting that Tom accepts the additional coverage without speaking with him first, because it is such a good deal and great coverage, he won’t mind. When Tom finds out what she has accepted on his behalf, without his knowledge, he is upset and wants to lodge a complaint to someone other than the insurance company and Monica; he wants to speak with an independent third party. He finds the contact information for the local regulatory authority. What are some of the responsibilities the regulatory authority has in protecting clients like Tom?

Justin decides to lease the personal vehicle of his friend Simon, who owns a window installation company. They agree on Justin having exclusive use of the vehicle in exchange for some renovations on Simon's house. What type of contract is this?

Ontario residents, Juan and Maria, are a married couple approaching retirement. They have asked their representative, Carlow, to review the details of Maria’s defined benefit plan (DBPP).

Which of the following statements about Maria's pension is CORRECT?

Angela works in a biomedical research lab where she has been assigned to discover possible antidotes to the anthrax virus. While the discovery process of testing possible antidotes would expose her to the deadly virus, she is excited about the assignment.

Knowing that anthrax can be contracted through infected food, air, or contact with skin, what risk management strategy would Angela employ by wearing protective gear over her mouth and skin?

Marietta receives a summons from the syndic of the CSF regarding an investigation into her associate. The summons was delivered to her office on May 2 and she took notice of it on May 4. The summons requires her to receive the syndic representative at her office on May 19 at 8:30 a.m. Marietta has already planned for and reserved a week off for a vacation abroad from May 15 to 22. She immediately emails the syndic representative to inform him that she will be out of the country and cannot be present on the 19th. She proposes meeting on the 14th or the 23rd of the same month. Pursuant to the Code of Ethics of the Chambre de la sécurité financière, which duties or obligations has Marietta breached?

Nathalie worked for 25 years as an administrative assistant at a manufacturing company. When she left the company 10 years ago, she transferred the money that she accumulated from the company’s pension plan into a locked-in retirement account (LIRA). Now she is 60 years of age and would like to withdraw the money from the LIRA.

Under which of the following circumstances would Nathalie be allowed to withdraw her funds?

Samya and Gary, who are both insurance representatives, are having lunch together. Gary has been very successful for several years and proposes a scheme to Samya to get insurance proposals signed for a fictional company they would create together. He believes that this system would make them millionaires in about ten years. Gary advises Samya to keep their conversation a secret. If Samya agrees to Gary’s proposal, what sanctions could she face?

Surjit and Rajbir got married in 2010, and Surjit named Rajbir as the irrevocable beneficiary of his life insurance contract. In 2017, the couple divorced amicably, and Surjit met with his insurance representative, Ivan, to review his plans. Surjit tells Ivan that he would like to keep Rajbir as his beneficiary.

What should Ivan counsel his client to do?

Insurance of persons advisor Somalia is careful to comply with the standards and regulations when she meets with potential clients. Under no circumstances would she want them to feel aggrieved or not respected. She makes sure to know their rights. Which legislation does Somalia not have to worry about?

Danny purchases a $1,000,000 whole life insurance policy. He names his three daughters, Donna-Joe, Stephanie, and Michelle, as revocable beneficiaries with each receiving one-third of the death benefit.

If Michelle predeceases Danny, and Danny did not have a chance to modify his beneficiary designation, how will Danny’s death benefit be paid out?

Paulette earns a modest income working as a delivery driver for FastFlowers Inc. in Quebec. The florist company has over 80 employees, 20 of whom are delivery drivers. The employees benefit from a group short- and long-term disability plan. One morning, while delivering flowers, Paulette's truck is struck by a bus. Paulette is taken to the hospital where a doctor deems that she will be unable to work for at least 4 months. Paulette contacts Jade, the human resources manager, to ask her who will pay her disability benefits.

Which of the following answers is CORRECT?

Gold, a financial security advisor, recently met with a wealthy client who needed tax advice. The client also wanted to draft a will and a mandate in case of incapacity. Eager to meet his client’s needs and make recommendations, he did not think it necessary to propose a meeting with the firm’s tax expert and notary. Towards whom has Gold breached his duties and obligations?

Harris is the father of Aden, Charlie, and Edmond. They are turning 29, 26, and 24 this year respectively. Harris purchased a life insurance policy with Aden as the life insured, Charlie as the successor owner, and Edmond as co-owner of the policy. He also named his wife, Becky, as the irrevocable beneficiary. Years have passed and the life insurance accumulated sufficient cash value. Harris is working out of town most of the time and none of the family members can get hold of him. One day, Harris encounters a car accident in another country and becomes unconscious. Becky and the children decide to cancel the policy and remit the cash value to Harris’s hospital. Which party can execute the intended transaction?

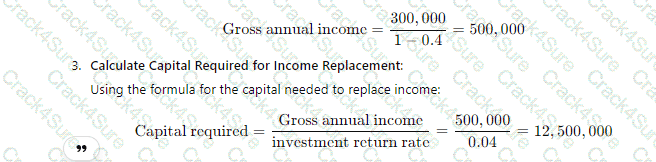

Jasper is the sole breadwinner in his family. His wife Stephanie has chosen to dedicate all of her time to raising their 3 young children. Luckily, Jasper earns a monthly after-tax income of $25,000 working as a family doctor in the local clinic. Jasper meets with his insurance agent Odda to purchase a life insurance policy that will ensure his family will be able to continue to enjoy their current lifestyle in the event of his death. If his average tax rate is 40% and the investment return is 4%, how much life insurance should Jasper purchase based on the income replacement approach?

Julie and Jim have been married for 16 years and decide to divorce. They draw up a list of property that will be partitioned based on the provisions of family patrimony: the family home, the cars, the RRSPs, and the benefits accrued with the RRQ during the marriage. What other items should be added to Julie and Jim's list?

Concilius has had a whole life (permanent) insurance policy for the past eight years. He decides he no longer wants this policy and stops paying the premiums. The cash value keeps the policy in effect for 28 months, after which it lapses. However, 46 months later, Concilius regrets his decision and applies to reinstate his policy. He is prepared to prove that he still meets the insurability conditions and to pay the overdue premiums plus interest, the cash value used, and the interest. Under what conditions will Concilius’ policy be reinstated?

Melissa, a La Tranquillité representative, is meeting with a client who tells her about something that happened to one of her friends. While she was taking part in an outdoor weekend at Mont-Tremblant Park, a forest fire broke out and one of the participants was never found. The client is about to take out life insurance with Melissa. She asks Melissa what would happen to her insurance capital in such a situation. What can Melissa tell the client?

Financial security advisor Juliette meets Pierre during a business meeting. Pierre gives her the name of a prospect, one of his friends. Juliette wants to start by contacting the prospect by email, then plans to follow up with a phone call to set up an appointment. Why should Juliette cease to proceed in this manner with her prospect?

Hussein wants to purchase a segregated fund. He has been following the news and believes the pharmaceutical sector will take off soon, and he wants to purchase a fund that will capitalize on his market view. He understands market fluctuations and is comfortable with the level of risk involved because he would only need to access these funds in 20 years.

Which of the following would be the most appropriate fund for Hussein?

(Julia deposited capital into an annuity contract that will start payments in three years and continue for 10 years. She is the annuitant; her son Ethan is the beneficiary.

What type of annuity has Julia purchased?)

(Gregory and Vanessa married at an early age and had three children, who are now in their forties: Eve, Rick and Max. When the couple retired five years ago, they purchased a joint life annuity. They also had a will drawn up naming the three children as equal beneficiaries of their estate. The will specifies that Eve will act as executor of the estate.

Last week, Gregory and Vanessa both died in a car accident.

Who could make a death claim as regards the annuity?)

Jack is excited to be joining his new employer, which offers group medical, dental, and retirement benefits to its employees. For his meeting with Human Resources, he brings his completed application form for medical and dental coverage, as well as a form to contribute to the GRRSP, since his employer matches contributions. The HR representative returns his application forms for group benefits to Jack and tells him that he is not eligible until certain conditions are met.

When might Jack become eligible?

Sasha is an employee at PranaTech. The company offers all employees a pension plan. PranaTech must contribute into the plan, but employee contributions are not mandatory. Sasha chooses where his funds will be invested.

Andrea, owner of Andrea’s Fashions Inc., employs her designer daughter Judy, who will carry on the business after Andrea is gone. Wishing to ensure that the business would not suffer financially when Andrea passes away, Andrea decides at age 50 to have her business own, pay for, and be the beneficiary of life insurance on Andrea's life. The type of insurance that best suits is non-convertible Term 10 life insurance renewable until age 80.

What should her life insurance agent advise regarding this policy?

(Joe and Joy, both aged 65, have $280,000 in savings and a $200,000 joint first-to-die life insurance policy. They want to buy an annuity to provide steady income in retirement.

What type of annuity would best suit their needs?)

(Dominique invested $25,000 in fixed-rate GICs and $25,000 in bond segregated funds.

What type of risk do these investments involve?)

Arianna, a healthy 61-year-old university professor, is retiring this year and wants to transfer the funds she accumulated in her registered retirement savings plan (RRSP) into an annuity. She is looking at different options and would like to know which of the following annuities will pay the highest monthly benefit.

Aadi is retiring from Scotia Grand, his employer of 25 years. While employed, Aadi benefitted from the company's deferred profit sharing plan (DPSP) and over the years, he accumulated $75,000.

Where should Aadi transfer these funds on a tax-deferral basis, now that he is retired?

Davy, who just turned 55, intends to retire 10 years from now. Together with his life insurance agent, he determines that he will need to have approximately $200,000 in RRSPs when he reaches age 65 in order to retire comfortably. He feels confident that his current RRSP account can generate a return of 3% per year on average for the next 10 years. However, he does not plan to contribute any new funds to his RRSP because he wants to start saving in his TFSA account instead. He therefore wonders whether his RRSP account currently has sufficient funds for him to meet his retirement goal in 10 years.

What is the minimum RRSP account balance needed now for Davy to meet his goal? (Round to the nearest dollar.)

(Justin purchased a single life annuity contract with no guaranteed period and no survivor benefit. He is now hospitalized.

If Justin passes away, who could make a claim on behalf of his estate regarding the annuity?)

Group insurance and group annuity representative Zaheb recently sold a group insurance contract to Alumo Inc., a company that employs about 50 plant employees. This is the first time the company offers such a plan. The employees are asking the company questions about how the prescription drug plan works. They are especially surprised to see that the plan covers very few of the brand name drugs often prescribed by their physicians. What should Zaheb do?

Lily works for Cloud 9 Inc. She earned $120,000 in Year 1 and $125,000 in Year 2. Lily contributes 5% of her income into a defined contribution pension plan (DCPP), and this contribution is matched by the employer. Lily has unused contribution room of $15,000 and wants to know how much she can contribute to her registered retirement savings plan (RRSP) in Year 2.

Christie’s savings and investment assets include the following:

RRSP: $100,000 in bond funds

Home valued at: $400,000

Defined benefit pension plan (DBPP) valued at: $50,000

Chequing account: $6,000

Savings account: $5,000

Her liabilities include:

Credit card debt: $20,000

Balance of mortgage: $200,000

Based on the information provided, what should Christie’s priority be?

Karine receives $200,000 from her mother's estate and decides to purchase an annuity. Her insurance agent Serge goes over her options with her, and she chooses the annuity that best suits her needs. Serge proceeds with the transaction.

Which of the following statements about the transaction is TRUE?

Sandrine, CEO of her own company for over 15 years, regularly consults you about the defined benefit pension plan she set up four years ago. Her company is going through unexpected difficulties, and she would like to know under which circumstances an employer can terminate such a plan (she is fully aware that this could go against employees’ expectations).

Which of the following answers are you most likely to give her?

Germaine, a shareholder-manager of a large firm, set up a group RRSP for her business several years ago. As the company has been very successful, she now wants to set up a second group savings plan for her employees. She would like this new plan to allow employees to withdraw money at any time without incurring additional income tax or other penalties.

Which one of the following plans would best fit Germaine’s requirements?

Remi owns a registered annuity contract that pays him a $2,500 monthly benefit. He purchased the contract five years ago from money he accumulated in his registered pension plan. At the time, he named his wife Annette as the revocable beneficiary of the contract. Today, he calls Louisa, his insurance agent, to designate his sister as beneficiary of the contract instead. Louisa tells him that there are restrictions on the contract and that he cannot change the beneficiary designation.

Why is Remi unable to make the change?

(Jorge meets with his new financial advisor. He brought a series of documents so that she can determine his investor profile.

Which of the following documents will not be helpful for determining Jorge’s investor profile?)

Larson, an insurance agent, meets with Julia, a real estate agent, to review her insurance needs. Julia has $500 in her savings account and does not own a tax-free savings account (TFSA) or registered retirement savings plan (RRSP). She earns an average of $150,000 a year in sales commissions and rental income from two condo units she owns. The combined value of her income properties is $1,000,000, and the mortgage is $200,000.

Larson recommends that Julia open a TFSA and use it to invest $400 a month in a money market fund.

Which of the following personal risks is Larson trying to mitigate with this advice?

Gaston’s wife died last month, leaving him a death benefit of $100,000 from her life insurance policy. Gaston, who is 60, wants to invest these funds in a safe investment that will mature when he retires at age 65 and thus provide him with added income. However, he wants to be able to easily withdraw funds at any time, if necessary. He would also like to be able to name his nephew as beneficiary.

What type of investment would best suit Gaston?

Brian is a machinist. For the past seven years, he’s worked for a company that offers a group benefits plan. Under that plan, the premiums for long-term disability coverage are entirely paid by the employees. Last year, an injury forced Brian to stop working for eight months. After a four-month waiting period, during which he collected Employment Insurance (EI) benefits, Brian received long-term disability (LTD) benefits from the group plan’s insurer. Brian is now preparing his income tax return and wonders about the tax implications of the different benefits he received while on disability. What statement accurately describes the tax treatment of Brian’s EI and LTD benefits?

Samira, a 42-year-old single mother of four, owns an individual disability insurance (DI) policy. Last week, she was hospitalized because of complications from diabetes. She hired an emergency nanny to care for her children until she was healthy enough to resume her normal activities. To her relief, Samira's DI policy contains a special rider that would cover up to $250 per day for these types of expenses.

What is the name of the rider contained in Samira's policy?

Arthur is a 79-year-old long-term care (LTC) policyholder whose daughter, Sheila, visits daily to help him get dressed and prepare meals. Sheila wants him to enter a nursing home because he isunable to dress himself. Though he cannot prepare his own meals, he can still feed himself, and once undressed, he can wash himself, seated in the bathtub.

Is Arthur eligible to receive LTC benefits?

Dorothy, age 36, is an architect. She runs her own office with the help of two assistants. She owns her own condo, has an active social life, and travels regularly for pleasure. She has a net annual income of approximately $125,000, once all the business, rent, salary, and car expenses have been paid. Dorothy is well aware of the significant financial problems that she would face for any absences from the office due to illness or disability. What are Dorothy’s main protection needs in this respect?

On February 15, 2015, Donald took out income replacement insurance with an accidental death and dismemberment rider of $50,000 and a critical illness insurance rider of $25,000. The policy wasissued on April 1, 2015. On April 10, 2015, his doctor tells him that the results of a urine analysis carried out at the end of March reveal a serious anomaly and refers him to an emergency urologist. On April 20, Donald is diagnosed with cancer of the right kidney, which is due to be removed on April 26. But, two days before the procedure, Donald dies in a car accident. What benefit amount will the estate receive?

Vladimir is a new insurance agent with Family-Assure Inc. He and his supervisor Petros are reviewing the information collected during Vladimir's first meeting with Vanessa, a restaurant owner looking to add to her existing disability insurance (DI) coverage. Petros notices an overlap among sources, although the existing coverage appears adequate. Petros reminds Vladimir to explain to Vanessa how she would be impacted if she were to claim disability benefits.

What should Vladimir tell Vanessa?

Marc, age 35, is a self-employed electrician. His annual income is approximately $60,000. His spouse Veronique works part-time and earns an annual income of $15,000. Marc and Veronique are parents of two young children. Their monthly financial obligations with regard to rent, car, clothing, and food amount to $3,000. What accident and sickness insurance protection do Marc and Veronique primarily need?

Tyler, a group insurance agent, is meeting with Yolanda, the director of his new group insurance client, Compact Funds Inc., to set up the company’s plan. Compact Funds employs over 30 employees, and Tyler recommends that they implement a contributory plan. Yolanda would like to understand what this means. Which of the following statements about contributory plans is CORRECT?

Diane is an insurance agent working for Gamma Insurance Inc. who is responsible for coaching a newly licensed agent, Wick. Wick has questions about his role, and he would like to know how he should service his clients.

What should Diane tell Wick about what is expected of him?

Ziad, aged 34, was an elementary school teacher for several years. However, staffing cutbacks and his love of food have prompted him to go into business. He just purchased a pizza franchise (taking a $150,000 personal loan to finance the venture) and entered into a five-year lease for his business. Ziad owns a 20-year term life insurance policy with a face amount of $250,000. He is also covered for some benefits under his wife’s group insurance plan, but knows he needs additional coverage. What type of accident and sickness coverage should Ziad purchase first?

Emery is a healthy wife and mother of two who spends her days caring for her children and volunteering at the local food bank. Emery would like to purchase disability insurance coverage because she is worried about how she would be able to take care of her family if she becomes disabled.

What type of disability policy, if any, is likely to be issued to her?

Anvi owns individual disability insurance that she purchased 5 years ago. At the time of application,she was a semi-professional boxer. Gamma Insurance Inc. offered her the disability policy with an exclusion stating that if she became disabled while boxing, the benefit would not be paid.

This week, while reviewing her insurance needs with Tyron, her insurance agent, she mentions that she retired from boxing and wants to know how, or if, this will affect her policy.

What should Tyron tell her?

Marsha and Alexis are equal partners in an advertising firm. They meet with Jose, an insurance agent, and Horacio, their lawyer, because they would like to protect themselves if one of them becomes disabled and unable to work for an extended period of time. At the end of their meeting, they agree to purchase $500,000 disability insurance policies on each other by each of them paying premiums.

What type of agreement do Marsha and Alexis have?

Monique meets with Tyra, an insurance agent, to review her insurance needs. Tyra explains the different types of policies and asks Monique for more information on her sources of income and expenses to properly evaluate her needs.

Which document should Tyra review to better understand Monique’s sources of income?

Rene, age 39, is a framing carpenter at a company that builds doors and windows. He has group disability insurance equivalent to 60% of his annual salary, which is $70,000. His monthly living expenses are $3,500. Since he has no pension plan at work, Rene has enrolled in an individual RRSP through payroll deductions ($1,000 per month). His RRSP savings currently amount to $45,000. In addition, Rene has $10,000 in a non-registered savings account. What should Rene’s life insurance agent advise him?

Patricia is a laboratory technician who normally earns $4,000 a month. A few months ago, she injured her leg rollerblading and was unable to work for four months. Since she owns a disability insurance policy with a residual benefit option, she received $2,400 a month from the insurer. Now that she is recovered, her doctor has cleared her to slowly return to work. Since she cannot work her regular full-time hours, her pay has decreased to $3,000 a month.

How much will she receive from her residual benefit when she returns to work?

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 09 Jul 2026

A close-up of a math Description automatically generated

A close-up of a math Description automatically generated