We at Crack4sure are committed to giving students who are preparing for the PRMIA 8006 Exam the most current and reliable questions . To help people study, we've made some of our Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition exam materials available for free to everyone. You can take the Free 8006 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

What is the fair price for a bond paying annual coupons at 5% and maturing in 5 years. Assume par value of $100 and the yield curve is flat at 6%.

Backwardation can be explained by:

Credit derivatives can be used for:

I. Reducing credit exposures

II. Reducing interest rate risks

III. Earn credit risk premiums

IV. Get market exposure without taking cash market positions

A zero coupon bond matures in 5 years and is yielding 5%. What is its modified duration?

It is January and an Australian importer needs to pay USD 1,120,000 at the end of August to a US creditor. If a AUD/USD futures contract is trading on the exchange at a futures price of 0.6750 (ie, 1 AUD = 0.6750 USD), and the contract size is USD 100,000, what would represent an appropriate hedge?

When hedging one fixed income security with another, the hedge ratio is determined by:

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the 2 year swap rate is 5%, and the yield curve is also flat at 5%

If the 3 month interest rate is 5%, and the 6 month interest rate is 6%, what would be the contract rate applicable to a 3 x 6 FRA?

What is the notional value of one equity index futures contract where the value of the index is 1500 and the contract multiplier is $50:

The price of a bond will approach its par as it approaches maturity. This is called:

Backwardation in commodity futures is explained by:

Which of the following relationships are true:

I. Delta of Put = Delta of Call - 1

II. Vega of Call = Vega of Put

III. Gamma of Call = Gamma of Put

IV. Theta of Put > Theta of Call

Assume dividends are zero.

What can the buyer of a 6 x 12 FRA expect to receive (or pay) if the contracted rate is 10% and the settlement rate is 12%? Assume contract notional is $100m.

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements are true for a contingent premium option:

I. They are also called 'pay-later' options

II. Premiums are due only if the option expires in the money

III. They are a combination of a vanilla option and an appropriate number of cash-or-nothing options

IV. They are preferred because the premiums are always less than those on equivalent vanilla options

Buying an option on a futures contract requires:

According to the dividend discount model, if d be the dividend per share in perpetuity of a company and g its expected growth rate, what would the share price of the company be. 'r' is the discount rate.

A pension fund has $100m in liabilities due in the future with an average modified duration of 20 years. The fund also holds a fixed income portfolio worth $125m with an average duration of 15 years. Which of the following approaches would be best suited for the pension fund to cover its interest rate risk?

What would be the expected return on a stock with a beta of 1.2, when the risk free rate is 3% and the broad market index is expected to earn 8%?

The most risky tranche of a structured credit derivative is called:

How will the Macaulay duration of a 10 year coupon bearing bond change if 10 year zero rates stay the same but the yield curve changes from being flat to upward sloping?

A refiner may use which of the following instruments to simultaneously protect against a fall in the prices of its products and a rise in the prices of its inputs:

Which of the following statements is true:

I. The standard deviation of a short position is the same as the standard deviation of a long position

II. The expected return of a short position is the same as that a long position in the same asset

III. If two assets are perfectly positively correlated, then a short position in one and a long position in the other are negatively correlated

IV. If we increase the weight of an asset in a portfolio, its correlation with other assets in the portfolio scales up proportionately

Which of the following expressions represents the Sharpe ratio, where ? is the expected return, ? is the standard deviation of returns, rm is the return of the market portfolio and if is the risk free rate:

Which of the following statements are true:

I. The swap rate, also called the swap spread, is initially calculated so that the value of the swap at inception is zero.

II. The value of a swap at initiation is different from zero and is equal to the difference between the NPV of the cash flows of the two legs of the swap

III. OTC swaps are standardized and limited to a defined set of standard contracts

IV. Interest rate and commodity swaps are the types of swaps that are most traded

Which of the following reflects the pricing convention for currency forwards, where one of the currencies is USD?

The effectiveness of a hedge is determined by which of the following expressions, where ?x,y is the correlation between the asset being hedged and the hedge position:

A)

B)

C)

D)

A portfolio comprising a long call and a short put option has the same payoff as:

Given identical prices, a bond trader prefers dealing with Bank A over Bank B. Given a choice between Bank B and Bank C, he prefers Bank B. Yet, when given a choice between Bank A and Bank C, he prefers dealing with Bank C. What axiom underlying the utility theory is he violating?

If the CHF/USD spot and 3 month (91 days) forward rates are 1.1763 and 1.1652, what is the annualized forward premium or discount?

A and B are two stocks with normally distributed returns. The returns for stock A have a mean of 5% and a standard deviation of 20%. Stock B has a mean of 3% and standard deviation of 5%. Their correlation is -0.6. What is the mean and volatility of a portfolio which holds stocks A and B in the ratio 6:4?

Where futures are being used to hedge a commodities position, which of the following formulae should be used to determine the number of futures contracts to buy (or sell)?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements is true:

I. American options can only be exercised at expiry

II. European options can be exercised at any time up to expiry

III. Bermudan options can be exercised at any time up to expiry except at certain times

IV. A European option can never be worth more than an American option

Which of the following statements are true:

I. Forward prices for a stock will fall if dividend expectations increase for the period the contract is alive

II. Three month forward prices will decline if the 10 year rate goes up, and short term rates stay unchanged

III. Futures exchanges require buyers but not sellers to deposit initial margins

IV. Variation margin is to be deposited when a futures contract is entered into

V. Futures exchanges requires hedgers and speculators to deposit identical margins

VI. Interest rate futures contracts carry duration but no convexity due to the daily cash settlements

Determine the enterprise value of a firm whose expected operating free cash flows are $100 each year and are growing with GDP at 2.5%. Assume its weighted average cost of capital is 7.5% annually.

Which of the following are true:

I. A interest rate cap is effectively a call option on an underlying interest rate

II. The premium on a cap is determined by the volatility of the underlying rate

III. A collar is more expensive than a cap or a floor

IV. A floor is effectively a put option on an underlying interest rate

If zero rates with continuous compounding for 4 and 5 years are 4% and 5% respectively, what is the forward rate for year 5?

Arrange the following rates in descending order, assuming an upward sloping yield curve:

1. The 10 year zero rate

2. The forward rate from year 9 to 10

3. The yield-to-maturity on a 10 year coupon bearing bond

Which of the following statements are true?

I. The square-root-of-time rule for scaling volatility over time assumes returns on different days are independent

II. If daily returns are positively correlated, realized volatility will be less than that calculated using the square-root-of time rule

III. If daily returns are negatively correlated, realized volatility will be less than that calculated using the square-root-of-time rule

IV. If stock prices are said to follow a random walk, it means daily returns are independent of each other and have an expected value of zero

It is January. Which of the following is an appropriate hedging strategy for a corn farmer expecting a harvest in June?

The risk of a portfolio that cannot be diversified away is called

If the implied volatility is known for a call option, what can be said about the implied volatility for a put option with the same strike and maturity?

A US treasury bill with 90 days to maturity and a face value of $100 is priced at $98. What is the annual bond-equivalent yield on this treasury bill?

A stock sells for $100, and a call on the same stock for one year hence at a strike price of $100 goes for $35. What is the price of the put on the stock with the same exercise and strike as the call? Assume the stock pays dividends at 1% per year at the end of the year and interest rates are 5% annually.

Which of the following statements are true:

I. The Kappa family of indices take only downside risk into account

II. The Treynor ratio provides information on the excess return per unit of specific risk

III. All else remaining constant, the Sharpe ratio for a portfolio will increase as we increase leverage by borrowing and investing in the risky bundle

IV. In the market portfolio, we can expect Jensen's alpha to equal zero.

Which of the following statements is INCORRECT according to CAPM:

If the delta of a call option is 0.3, what is the delta of the corresponding put option?

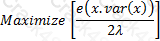

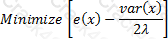

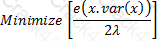

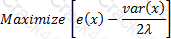

The objective function satisfying the mean-variance criterion for a gamble with an expected payoff of x, variance var(x) and coefficient of risk tolerance is ? is:

A)

B)

C)

D)

A 'short squeeze' refers to a situation where

Calculate the basis point value, or PV01, of a bond with a modified duration of 5 and a price of $102.

An investor expects stock prices to move either sharply up or down. His preferred strategy should be to:

Which of the following best describes a 'when-issued' market?

According to the CAPM, the beta of a risky asset depends upon:

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the current zero coupon bond yields for 1, 2 and 3 years are 5%, 6% and 7% respectively. Also assume that the yield curve stays the same after two years (ie, at the end of year two, the rates for the following three years are 5%, 6%, and 7% respectively).

What would be the total all in price payable on an 5% annual coupon bond quoted at a clean price of $98, where the settlement date is 60 days after the latest coupon payment. Use Act/360 day basis.

An asset has a volatility of 10% per year. An investment manager chooses to hedge it with another asset that has a volatility of 9% per year and a correlation of 0.9. Calculate the hedge ratio.

Which of the following will have the effect of increasing the duration of a bond, all else remaining equal:

I. Increase in bond coupon

II. Increase in bond yield

III. Decrease in coupon frequency

IV. Increase in bond maturity

What is the delta of a forward contract on a non-dividend paying stock?

Credit risk in the case of a CDO (Collateralized Debt Obligation) is borne by:

The rule that optimal portfolios will maximize the Sharpe ratio only applies when which of the following conditions is satisfied:

I. It is possible to borrow or lend any amounts at the risk free rate

II. Investors' risk preferences are fully described by expected returns and standard deviation

III. Investors are risk neutral

What is the day count convention used for US government bonds?

In terms of notional values traded, which of the following represents the largest share of total traded futures and options globally?

A risk manager is deciding between using futures or forward contracts to hedge a forward foreign exchange position. Which of the following statements would be true as he considers his decision:

I. He would need to consider tailing the hedge for the futures contracts while that does not apply to forward contracts

II. He would need to consider tailing the hedge for the forward contract while that does not apply to futures contracts

III. He would need to consider counterparty risk for the futures contracts while that is unlikely to be an issue for the forward contract

IV. He would be likely able to match up maturity dates to his liability when using futures while that may not be so for the forward contracts

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following best describes a shout option

A 15 year bond is trading at par. Its modified duration is 11 years and convexity is 80. Determine the price of the bond following a 10 basis point increase in interest rates

A borrower who fears a rise in interest rates and wishes to hedge against that risk should:

Which of the following statements is true:

I. A high market beta implies a high degree of correlation with the market

II. Correlation coefficient and covariance between assets have the same sign

III. A correlation of zero indicates the absence of a linear relationship between the two assets

IV. Unless assets are perfectly correlated, diversification always reduces portfolio risk.

Which of the following markets are characterized by the presence of a market maker always making two-way prices?

A hedge fund offers a fund with an expected volatility of 12% and expected returns of 12%. The risk free rate is 4%. An institutional investor wants the hedge fund manager to invest 60% of their total allocation to the fund, and the rest in the risk free asset. What expected return and volatility can the institutional investor expect?

Which of the following describes the efficient frontier most accurately?

Repos are used for:

I. Short term borrowings

II. Managing credit risk exposures

III. Money market operations by central banks

IV. Facilitating short positions

Theta for a call option:

If the spot price for a commodity is lower than the forward price, the market is said to be in:

What is the price of a treasury bill with $100 face maturing in 90 days and yielding 5%?

What is the approximate delta of an exactly at-the-money call option?

Which of the following assumptions underlie the 'square root of time' rule used for computing volatility estimates over different time horizons?

I. asset returns are independent and identically distributed (i.i.d.)

II. volatility is constant over time

III. no serial correlation in the forward projection of volatility

IV. negative serial correlations exist in the time series of returns

A bond pays semi-annual coupons at an annual rate of 10%, and will mature in a year. What is its modified duration? Assume the yield curve is flat for the next 12 months at 5%.

Which of the following statements are true in respect of a fixed income portfolio:

I. A hedge based on portfolio duration is valid only for small changes in interest rates and needs periodic readjusting

II. A duration based portfolio hedge can be improved by making a convexity adjustment

III. A long position in bonds benefits from the resulting negative convexity

IV. A duration based hedge makes the implicit assumption that only parallel shifts in the yield curve are possible

Which of the following expressions represents the Treynor ratio, where ? is the expected return, ? is the standard deviation of returns, rm is the return of the market portfolio and rf is the risk free rate:

A)

B)

C)

D)

According to the mean-variance criterion, which of the following statements are true in relation to an investor who does not borrow or lend?

I. The investor would select a portfolio of assets to minimize drawdowns

II. The investor would prefer a portfolio on the efficient frontier

III. The investor would prefer a portfolio with a higher return given the same level of risk

IV. The investor would maximize portfolio return alone as the mean-variance criterion assumes risk neutrality

Which of the following statements are true for a portfolio of two assets:

I. Given volatility, weights and correlation, combined standard deviation cannot be calculated without additional information on covariances.

II. When the two assets are perfectly negatively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

III. When the two assets are uncorrelated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

IV. When the two assets are perfectly positively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

Which of the following statements is not true about covered calls on stocks

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 10 Jul 2026

103.04.e2

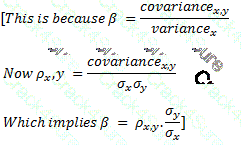

103.04.e2 103.04.e2, where x is the market portfolio and y is the asset under consideration.

103.04.e2, where x is the market portfolio and y is the asset under consideration. 103.04.e

103.04.e{kind=link}