We at Crack4sure are committed to giving students who are preparing for the CIMA F1 Exam the most current and reliable questions . To help people study, we've made some of our Financial Reporting exam materials available for free to everyone. You can take the Free F1 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

Which of the following is a condition that has to be met for an entity to be exempt the requirement to prepare consolidated financial statements?

To apply the fundamental principles of the Code of Ethics, existing and potential threats to the entity first need to be identified and evaluated.

Which THREE of the following are identified in the Code as threats?

An entity opens a new factory and receives a government grant of $25,000 towards the cost of new plant and equipment. This new plant and equipment originally costs $100,000.

The entity uses the net cost method allowed by IAS 20 Accounting for Government Grants and Disclosure of Government Assistance to record government grants of this nature. All plant and equipment is depreciated at 20% a year on a straight line basis.

Calculate the amount of depreciation to be included for this plant and equipment in the statement of profit of loss for the factory's first year of operation.

Give your answer to the nearest whole $.

What does the exemption method of giving double taxation relief mean?

Which of the following is NOT a principle in the CIMA Code of Ethics for Professional Accountants?

JKL prepares its financial statements to 31 December each year. For the year ended 31 December 20X5 inventory was held for 76 days on average.

The directors of JKL decide to reduce the average inventory level to $6.5 million from 1 January 20X6 JKL's revenue for 20X6 is $54 million on which a gross profit margin of 20% is earned.

Assuming that the average receivables and payables days remain constant what will be the effect of the expected reduction in inventory on JKL's working capital cycle for the year ended 31 December 20X6?

EFG prepares financial statements to 31 December each year. EFG has the following receivable days based on the year end receivable balances:

Which of the following would be a reason for this decrease in receivable days?

When calculating the gam chargeable to tax on the disposal of a building, which of the following would NOT be an allowable deduction?

Entity T operates within several countries, but its country of residence is Country F. In 20X5, Entity T made $8.4 million in Country M. Country M has a flat rate corporation tax of 5.9%.

Country F and Country M operate a double taxation treaty which uses a foreign tax credit system. In Country F, there is a tax of 10% tax on all foreign income.

Taking into account the credit, what is the total tax liability that Entity T owes on its Country M income, in Country F?

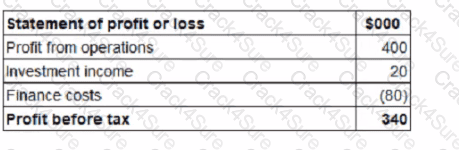

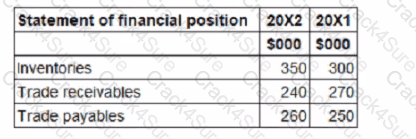

Below are extracts from LLL's financial statements for the year ended 31 December 20X2.

Depreciation of $25,000 was charged on properly, plant and equipment in the year and there were no disposals

What is the cash generated from operations for inclusion in LLL's statement of cash flows for the year ended 31 December 20X2?

Which of the following would NOT be a risk or impact of overtrading?

DE purchased an asset on 1 January 20X1 for $60,000 with a useful economic life of six years and a residual value of $3,000.

DE uses straight line depreciation for this asset.

On 31 December 20X3 the asset has a value in use of $ $28,000 and a fair value of $26,000.

Which of the following values should be used for the asset in DE's statement of financial position as at 31 December 20X3?

The legislation in Country S provides for an indexation allowance in the calculation of capital tax. STU operates in Country S where the indexation factor for the period 1 January 20X1 to 31 December 20X6 is 20%

STU purchased a building for $64,000 on 1 January 20X1, incurring legal fees of $4,000. STU sold the building for $86,000 on 31 December 20X6 before selling fees of $3,500

What is the chargeable capital gam arising on STU's disposal of the building?

In accordance with The Conceptual Framework for Financial Reporting, faithful representation is a fundamental qualitative characteristic.

To be a faithful representation financial information must be as far as possible which THREE of the following?

Which of the following would NOT be assessed for tax under a Pay-As-You-Earn system?

Which of the following methods could be used by a tax authority to reduce tax evasion and avoidance?

According to IAS 21 The Effects of Changes in Foreign Exchange Rates, an entity should determine its functional currency.

Which of the following is NOT a factor that should be considered by an entity when determining its functional currency?

Statements of financial position for FG, IJ and KL at 31 December 20X5 include the following balances:

FG acquired 90% of IJ's equity shares for $358,000 on 1 July 20X5 when IJ's retained earnings were $98,000.

FG acquired 100% of KL's equity shares for $360,000 on 1 January 20X5 when KL's retained earnings were $155,000.

FG used the proportion of net assets method to value non-controlling interests at acquisition.

KL sold a piece of land to FG for $130,000 on 1 September 20X5. At the date of transfer the land had a carrying value of $50,000.

The management of FG expect KL to make profits in the future and no impairment ot its goodwill was proposed at 31 December 20X5.

Calculate the amount of retained earnings that will be included in FG's consolidated statement of financial position as at 31 December 20X5.

Give your answer to the nearest whole $.

Which of the following would be capitalized as an intangible asset in accordance with IAS 38 Intangible Assets?

Statements of financial position for YZ, BC and DE at 31 March 20X2 include the following balances:

YZ purchased 90% of BC's equity shares for $508,000 on 1 January 20X2. On 1 January 20X2 BC's retained earnings were $183,000. YZ uses the proportion of net assets method to value non-controlling interest at acquisition.

YZ purchased 30% of DE's equity shares on 1 April 20X1 for $112,000. DE's retained earnings at 1 April 20X1 were $88,000.

On 1 February 20X2 YZ sold goods to BC for $28,000 at a mark up of 25% on cost. All the goods were still in BC's inventory at 31 March 20X2.

Calculate the goodwill arising on the acquisition of BC.

Give your answer to the nearest whole $.

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September 20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

What is the revenue figure to be included in PQ's consolidated statement of profit or loss for the year ended 31 December 20X0?

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1.

Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year's depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ's property.

The total depreciation charge for property, plant and equipment in ZZ's statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ's statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3.

What cash outflow figure should be included within cash flows from investing activities for the purchase of property, plant and equipment?

Which of the following would NOT be classified as part of non-current assets in a statement of financial position?

Which THREE of the following would be included in a cash budget?

The following information is extracted from OO's statement of financial position at 31 March:

Included in other payables is interest payable of $80,000 at 31 March 20X2 and $73,000 at 31 March 20X1.

The following information if included within OO's statement of profit or loss for the year ended 31 March 20X2:

Included within finance cost is $124,000 which relates to interest paid on a finance lease. 00 includes finance lease interest within financing activities on its statement of cash flows.________________

Within OO's statement of cash flow for the year ended 31 March 20X2 which figures should be included to reflect the changes in working capital within the net cash flow from operating activities?

Country X charges corporate income tax at the rate of 20% on all income irrespective of whether it is paid out as a dividend. Country Y charges corporate income tax at the rate of 25% on all income.

An entity, AA, which is resident in Country X pays a dividend of $100,000 to another entity, BB, which is resident in Country Y.

Countries X and Y have a double taxation treaty which adopts the exemption method in respect of this type of transaction.

What is BB's liability to tax in Country Y in respect of the dividend income received?

Identify whether the scenarios below are examples of tax evasion or tax avoidance, by placing either tax evasion of tax avoidance against each one.

If a parent entity is to be exempt from preparing consolidated financial statements it needs to satisfy certain conditions according to IFRS 10 Consolidated Financial Statements.

Which TWO of the following are conditions that need to be satisfied to be exempt?

The following information is extracted from the trial balance of YY at 30 September 20X3.

i. Included in revenue is a refundable deposit of $20 million for a sales transaction that is due to take place on 14 October 20X3.

ii. The cost of closing inventory is $28 million, however, the net realisable value is estimated at $25 million.

iii. The interest free loan was obtained on 1 January 20X3. The loan is repayable in 12 quarterly installments starting on 31 March 20X3. All installments to date have been paid on time.

Calculate the cost of sales that would be shown in YY's statement of profit or loss for the year ended 30 September 20X3.

Give your answer to the nearest $ million.

An entity's policy is to finance the investment in working capital using short-term financing to fund all of its investment in fluctuating net current assets as well as some of its investment in permanent net current assets.

What is this working capital financing policy known as?

An entity acquires 100% of the equity shares in another entity.

The consideration paid for the shares is less than the fair value of the net assets acquired.

Which of the following is the correct accounting treatment for the difference between the consideration paid and the fair value of the net assets acquired, in accordance with IFRS 3 Business Combinations?

The auditor has identified a material but not pervasive mis-statement whilst undertaking the external audit of an entity's financial statements.

This will result in a modified audit report with the opinion being .

While conducting their audit, auditor 0 did not encounter issues which significantly limited the scope of their audit, however they did run into problems in that they disagreed with the management on facts in the

statements.

These disagreements were somewhat material, but they did not affect the auditor's overall opinion of the business. Which of the following statements should auditor 0 issue?

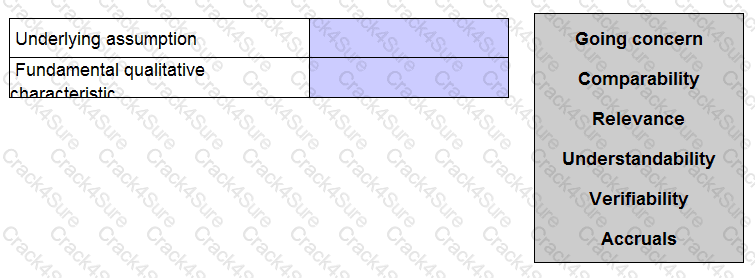

The Conceptual Framework for Financial Reporting issued by the International Accounting Standards Board (known as the IASB's conceptual framework) includes one underlying assumption about the preparation of financial statements and two fundamental qualitative characteristics for financial information.

Identify the underlying assumption and one of the fundamental characteristics by placing one of the options in each of the boxes below.

Entity RH has an recognised a taxable profit of $1.Smillion for 20X1'. In Entity RH's resident country. Country M, depreciation charges and entertaining expenses are disallowed expenses. Below is some information on

Entitry RH's outgoings for the period:

Depreciation charged on PPE: $450,000

Political donations: $155,000

Staff parties: $3,200

Cost of updating assets: $10,000

Other expenses: $83,500

In Country M, there is a standard corporation tax of 12% charged on all corporation profits. What is Entity RH's total tax liability for this period?

PP supplies zero-rated and standard-rated goods. During the year ended 30 March 20X3, the standard-rated goods made up 50% of the total supplies. During the year ended 30 March 20X4 this percentage increased to 60%.

What percentage of input tax suffered can PP claim back in the year ended 30 March 20X4?

Give your answer as a whole number.

Country X levies corporate income tax at a rate of 25% and charges income tax on all profits irrespective of whether they are distributed by way of dividend. Country Y levies corporate income tax at a rate of 20%.

A, who is resident in Country X, pays a divided to B, who is resident in Country Y. B is required to pay corporate income tax on the dividend received from A, but a deduction can be made for the tax suffered on this dividend restricted to a rate of 20%.

Which method of relief for foreign tax does this describe?

Which of the following are techniques that can be used by a company to ensure they receive timely payment of receivables? Select ALL that apply:

AB sells to ST, a group entity, 10,000 units at $2.50 each. The market value was $6 each.

The effect on AB of the transfer pricing legislation on this transaction would be to: .

The United Kingdom (UK) uses a principle based approach to corporate governance which means:

The following data relates to Company AB.

Statement of Profit or Loss for the year ended 30 June 20X4:

During the year ending 30 June 20X4, which was not a leap year, the average stock holding period was 102 days.

Calculate the working capital cycle in days.

Give your answer to the nearest full day.

Country A permits the following deductions in an entity's annual corporate income tax return in relation to entertaining expenses and gifts;

1 Employee entertaining up to a value of $150 a head

2 Entertaining of overseas customers.

3 Individual gifts not to exceed $10 in value

Which THREE of the following actions would be regarded as tax evasion?

Which TWO of the following are features of a bank overdraft?

In accordance with IFRS 3 Business Combinations, acquisition accounting of an investment in another entity within the consolidated statement of financial position means that the:

Country X levies a duty on alcoholic drinks. Where the alcohol content is above 40% by volume the duty levied is $5 per 1 litre bottle.

What type of tax is this duty?

EF has been offering its customers a 60 day credit period, but now wants to improve its cash flow.

EF is proposing to offer a 2% discount for payment in 15 days.

Assume a 365 day year and an invoice value of $100.

Which of the following is the effective annual interest rate EF will incur for this action?

OP is considering investing in government bonds. The current price of a $100 bond with 8 years to maturity is $88.

The bonds have a coupon rate of 6% and repay face value of $100 at the end of the 8 years.

Calculate the yield to maturity.

Give your answer to one decimal place.

OP holds an investment property purchased on 1 January 20X3 for $700,000 with a useful economic life of 25 years.

At 31 December 20X5 the fair value of the investment property was $750,000 with a revised useful economic life of 25 years from that date.

OP has been carrying the investment property using the cost model until 31 December 20X5.

The directors wish to change their valuation method to fair value in accordance with IAS 40 Investment Property.

Which of the following is the correct treatment of the revaluation gain and the value of the property in the statement of financial position at 31 December 20X5?

Which THREE of the following are principles identified by the Code of Ethics?

During the year a piece of equipment that originally cost $96,000, with accumulated depreciation of $39,000, met the criteria of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations to be classified as held for sale.

The equipment is being advertised for sale at $46,000 and costs of $1,000 will be incurred to enable the sale to be completed.

At what value should the equipment be included in the statement of financial position at the year end assuming that it remains unsold?

Give your answer to the nearest whole number.

When a trading loss is incurred by an entity, the entity may be able to claim loss relief. The way in which loss relief is claimed vanes from country to country.

Which of the following is NOT normally a way of claiming loss relief for a trading loss?

Which THREE of the following are conditions that must be met to allow an asset to be categorised as held for sale?

Which THREE of the following are included in the International Accounting Standards Board's "The Conceptual Framework for Financial Reporting"?

The IV Group is formed of I Ltd and its subsidiary company V Ltd. I Ltd purchased 67% of V Ltd's ordinary share capital on 31 March 20X3.

The purchase cost I Ltd £129,000. At the date of purchase V Ltd's net assets were £155,000 while its share capital was £37,000. NCI fair value on the date of acquisition was £31,000.

What was the amount of goodwill I Ltd paid as part of the acquisition. Calculate this figure using both the proportion of net assets method and the full good will method for valuing the non-controlling interest.

Mr K is being pressured by his manager to change figures in his report so that it will improve his manager's bonus.

His manager has promised Mr K a promotion if he agrees to do this.

What threats is Mr K facing?

MNO is a commercial bank. One of MNO's clients is FGH, a trading company which sells goods to PQR.

MNO is asked to draw up an instrument between FGH and PQR in respect of goods sold FGH then asks MNO to sell this instrument on its behalf in the discount market MNO does this and pays the proceeds to FGH.

What source of short-term finance is being described here?

Country J is a newly formed independent country and it's accounting professionals are considering adopting international financial reporting standards (IFRS).

Which of the following is a disadvantage to Country J of adopting IFRS as their local generally accepted accounting practice (GAAP)?

Whilst undertaking an external audit, the auditor has identified that there is insufficient evidence to support the financial statements.

As a result the auditors consider these financial statements to be wholly unreliable for decision making purposes.

This will result in a modified audit report with the opinion being .

Which of the following is NOT a source of short-term finance?

ABC has the following working capital ratios at 31 December 20X2:

During the year ended 31 December 20X4 credit purchases were $1,700,000 and at 31 December 20X4 the outstanding trade payables balance was $340,000

During the year ended 31 December 20X4 credit purchases were $1,700,000 and at 31 December 20X4 the outstanding trade payables balance was $340,000

Calculate the working capital cycle for ABC.

Give your answer to the nearest whole number of days and assume there are 365 days in a year.

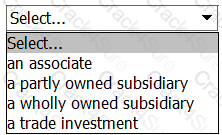

FG purchased 40% of the equity shares of QR and exerted significant influence over the board of the directors.

QR will be classified as____of FG.

Which THREE of the following matters should an entity consider when determining the credit terms granted to a customer?

An asset cost $250,000 on 1 January 20X1 and on that date was assessed to have a residual value of $40,000 and a useful economic life of six years. On 1 January 20X4 management assessed that the remaining useful economic life of the asset was five years and that the asset had a residual value of nil.

What is the depreciation charge for this asset in the year ended 31 December 20X4?

Give your answer to the nearest whole number.

The International Accounting Standards Board's "The Conceptual Framework for Financial Reporting" identifies fundamental and enhancing qualitative characteristics of financial statements.

Which of the following is included within the fundamental characteristics?

KL has just completed their inventory count and has ascertained that the cost value of the inventory is $460,000; this was made up of 10,000 units of component part FF.

A week before the year end the FF components were moved to a temporary warehouse.

Two weeks later they were inspected and found to have been damaged by the damp conditions in the temporary warehouse.

Of the 10,000 units 2,500 of them were damaged. After remedial work of $5.00 per unit KL anticipates they will be able to sell the damaged parts for $32.00 per unit.

What is the value for closing inventory to be included in the financial statements of KL?

Give your answer to the nearest $.

Company Y is using some of the money from a share issue to purchase a new office building. The company is also using some of the money to purchase inventories. Which method of financing is this?

On 1 January 20X6 PQR leases equipment for 3 years to use on a construction project. The total lease payments are $360,000 divided into 36 monthly instalments of $10,000 On 1 January 20X6 the present value of the lease payments is $270,000 and initial direct costs of $3,000 were incurred.

Which THREE of the following statements are true?

AA manufactures computers. These are sold to BB at $100 a computer plus a 5% sales tax. BB subsequently sells the computers to CC for $200 a computer plus a 5% sales tax. C sells the computers to customers at $300 a computer plus a 5% sales tax.

The total tax received by the tax authority is $30.

Which type of tax is described above?

Which of the following is NOT a feature of a multi-stage sales tax?

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 10 Jul 2026