We at Crack4sure are committed to giving students who are preparing for the PRMIA 8008 Exam the most current and reliable questions . To help people study, we've made some of our PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition exam materials available for free to everyone. You can take the Free 8008 Practice Test as many times as you want. The answers to the practice questions are given, and each answer is explained.

Which of the following are valid objectives of a reverse stress test:

I. Ensure that a firm can survive for long enough after risks have materialized for it to either regain market confidence, restructure or be sold, or be closed down in an orderly manner,

II. Discover the vulnerabilities of the current business plan,

III. Better integrate business and capital planning,

IV. Create a 'zero-failure' environment at the systemic level in the financial sector

In respect of operational risk capital calculations, the Basel II accord recommends a confidence level and time horizon of:

Which of the following measures can be used to reduce settlement risks:

Which of the following carry greater counterparty risk: a forward contract on a 10 year note, or a commercial paper carrying a AA credit rating with identical maturity and notional?

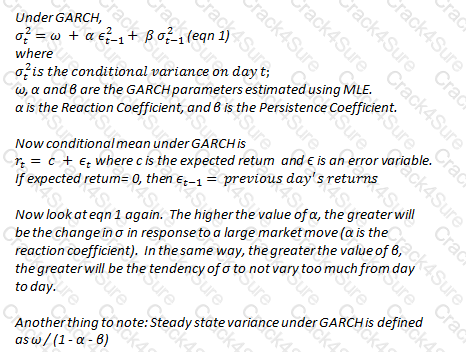

What is the annualized steady state volatility under a GARCH model where alpha is 0.1, beta is 0.8 and omega is 0.00025?

In estimating credit exposure for a line of credit, it is usual to consider:

When performing portfolio stress tests using hypothetical scenarios, which of the following is not generally a challenge for the risk manager?

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel II operational risk categories as:

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

Which of the following does not affect the credit risk facing a lender institution?

Which of the following statements are true:

I. Heavy tailed parametric distributions are a good choice for severity modeling in operational risk.

II. Heavy tailed body-tail distributions are a good choice for severity modeling in operational risk.

III. Log-likelihood is a means to estimate parameters for a distribution.

IV. Body-tail distributions allow modeling small losses differently from large ones.

Which of the following is a cause of model risk in risk management?

Loss provisioning is intended to cover:

An equity manager holds a portfolio valued at $10m which has a beta of 1.1. He believes the market may see a dip in the coming weeks and wishes to eliminate his market exposure temporarily. Market index futures are available and the current futures notional on these is $50,000 per contract. Which of the following represents the best strategy for the manager to hedge his risk according to his views?

Which of the formulae below describes incremental VaR where a new position 'm' is added to the portfolio? (where p is the portfolio, and V_i is the value of the i-th asset in the portfolio. All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

Which of the following represent the parameters that define a VaR estimate?

The standalone economic capital estimates for the three uncorrelated business units of a bank are $100, $200 and $150 respectively. What is the combined economic capital for the bank?

Which of the following statements is a correct description of the phrase present value of a basis point?

Which of the following statements are true:

I. Pre-settlement risk is the risk that one of the parties to a contract might default prior to the maturity date or expiry of the contract.

II. Pre-settlement risk can be partly mitigated by providing for early settlement in the agreements between the counterparties.

III. The current exposure from an OTC derivatives contract is equivalent to its current replacement value.

IV. Loan equivalent exposures are calculated even for exposures that are not loans as a practical matter for calculating credit risk exposure.

For a loan portfolio, unexpected losses are charged against:

Which of the following statements are true ?

I. Risk governance structures distribute rights and responsibilities among stakeholders in the corporation

II. Cybernetics is the multidisciplinary study of cyber risk and control systems underlying information systems in an organization

III. Corporate governance is a subset of the larger subject of risk governance

IV. The Cadbury report was issued in the early 90s and was one of the early frameworks for corporate governance

For a security with a daily standard deviation of 2%, calculate the 10-day VaR at the 95% confidence level. Assume expected daily returns to be nil.

Which of the following statements are true:

I. Credit VaR often assumes a one year time horizon, as opposed to a shorter time horizon for market risk as credit activities generally span a longer time period.

II. Credit losses in the banking book should be assessed on the basis of mark-to-market mode as opposed to the default-only mode.

III. The confidence level used in the calculation of credit capital is high when the objective is to maintain a high credit rating for the institution.

IV. Credit capital calculations for securities with liquid markets and held for proprietary positions should be based on marking positions to market.

If the annual default hazard rate for a borrower is 10%, what is the probability that there is no default at the end of 5 years?

All else remaining the same, an increase in the joint probability of default between two obligors causes the default correlation between the two to:

Altman's Z-score does not consider which of the following ratios:

If F be the face value of a firm's debt, V the value of its assets and E the market value of equity, then according to the option pricing approach a default on debt occurs when:

When compared to a high severity low frequency risk, the operational risk capital requirement for a low severity high frequency risk is likely to be:

Which of the following data sources are expected to influence operational risk capital under the AMA:

I. Internal Loss Data (ILD)

II. External Loss Data (ELD)

III. Scenario Data (SD)

IV. Business Environment and Internal Control Factors (BEICF)

If the odds of default are 1:5, what is the probability of default?

In January, a bank buys a basket of mortgages with a view to securitize them by April. Due to an unexpected lack of investors in the securitization market, it is unable to do so and is left with the exposure to the mortgages on its books. This is an example of:

If the marginal probabilities of default for a corporate bond for years 1, 2 and 3 are 2%, 3% and 4% respectively, what is the cumulative probability of default at the end of year 3?

Which of the following are true:

I. Monte Carlo estimates of VaR can be expected to be identical or very close to those obtained using analytical methods if both are based on the same parameters.

II. Non-normality of returns does not pose a problem if we use Monte Carlo simulations based upon parameters and a distribution assumed to be normal.

III. Historical VaR estimates do not require any distribution assumptions.

IV. Historical simulations by definition limit VaR estimation only to the range of possibilities that have already occurred.

What would be the correct order of steps to addressing data quality problems in an organization?

In setting confidence levels for VaR estimates for internal limit setting, it is generally desirable:

Which of the following should be included when calculating the Gross Income indicator used to calculate operational risk capital under the basic indicator and standardized approaches under Basel II?

The Basel framework does not permit which of the following Units of Measure (UoM) for operational risk modeling:

I. UoM based on legal entity

II. UoM based on event type

III. UoM based on geography

IV. UoM based on line of business

When fitting a distribution in excess of a threshold as part of the body-tail distribution method described by the equation below, how is the parameter 'p' calculated.

Here, F(x) is the severity distribution. F(Tail) and F(Body) are the parametric distributions selected for the tail and the body, and T is the threshold in excess of which the tail is considered to begin.

Which of the following is a most complete measure of the liquidity gap facing a firm?

The loss severity distribution for operational risk loss events is generally modeled by which of the following distributions:

I. the lognormal distribution

II. The gamma density function

III. Generalized hyperbolic distributions

IV. Lognormal mixtures

Which of the following will be a loss not covered by operational risk as defined under Basel II?

Under the contingent claims approach to measuring credit risk, which of the following factors does NOT affect credit risk:

The risk that a counterparty fails to deliver its obligation upon settlement while having received the leg owed to it is called:

Which of the following is not true about the ISDA master agreement (ISDA MA):

Which of the following are valid approaches to leveraging external loss data for modeling operational risks:

I. Both internal and external losses can be fitted with distributions, and a weighted average approach using these distributions is relied upon for capital calculations.

II. External loss data is used to inform scenario modeling.

III. External loss data is combined with internal loss data points, and distributions fitted to the combined data set.

IV. External loss data is used to replace internal loss data points to create a higher quality data set to fit distributions.

Which of the following credit risk models relies upon the analysis of credit rating migrations to assess credit risk?

If E denotes the expected value of a loan portfolio at the end on one year and U the value of the portfolio in the worst case scenario at the 99% confidence level, which of the following expressions correctly describes economic capital required in respect of credit risk?

Which of the following are measures of liquidity risk

I. Liquidity Coverage Ratio

II. Net Stable Funding Ratio

III. Book Value to Share Price

IV. Earnings Per Share

Which of the following are valid techniques used when performing stress testing based on hypothetical test scenarios:

I. Modifying the covariance matrix by changing asset correlations

II. Specifying hypothetical shocks

III. Sensitivity analysis based on changes in selected risk factors

IV. Evaluating systemic liquidity risks

A risk analyst uses the GARCH model to forecast volatility, and the parameters he uses are ? = 0.001%, ? = 0.05 and ? = 0.93. Yesterday's daily volatility was calculated to be 1%. What is the long term annual volatility under the analyst's model?

For a corporate issuer, which of the following can be used to calculate market implied default probabilities?

I. CDS spreads

II. Bond prices

III. Credit rating issued by S&P

IV. Altman's scoring model

If a borrower has a default probability of 12% over one year, what is the probability of default over a month?

A loan portfolio's full notional value is $100, and its value in a worst case scenario at the 99% level of confidence is $65. Expected losses on the portfolio are estimated at 10%. What is the level of economic capital required to cushion unexpected losses?

Which of the following is additive, ie equal to the sum of its components

Which of the following represents a riskier exposure for a bank: A LIBOR based loan, or an Overnight Indexed Swap? Which of the two rates is expected to be higher?

Assume the same counterparty and the same notional.

Which of the following statements is true:

I. Expected credit losses are charged to the unit's P&L while unexpected losses hit risk capital reserves.

II. Credit portfolio loss distributions are symmetrical

III. For a bank holding $10m in face of a defaulted debt that it acquired for $2m, the bank's legal claim in the bankruptcy court will be $10m.

IV. The legal claim in bankruptcy court for an over the counter derivatives contract will be the notional value of the contract.

Which of the following is not a credit event under ISDA definitions?

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

An assumption regarding the absence of ratings momentum is referred to as:

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank's defaults are independent of each other, with a probability of default of 0.05 each. The BHC's probability of default is 0.11.

What is the probability of default of both the BHC and the investment bank? What is the probability of the BHC's default provided both the investment bank and the retail bank survive?

The estimate of historical VaR at 99% confidence based on a set of data with 100 observations will end up being:

When modeling severity of operational risk losses using extreme value theory (EVT), practitioners often use which of the following distributions to model loss severity:

I. The 'Peaks-over-threshold' (POT) model

II. Generalized Pareto distributions

III. Lognormal mixtures

IV. Generalized hyperbolic distributions

The daily VaR of an investor's commodity position is $10m. The annual VaR, assuming daily returns are independent, is ~$158m (using the square root of time rule). Which of the following statements are correct?

I. If daily returns are not independent and show mean-reversion, the actual annual VaR will be higher than $158m.

II. If daily returns are not independent and show mean-reversion, the actual annual VaR will be lower than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be higher than $158m.

III. If daily returns are not independent and exhibit trending (autocorrelation), the actual annual VaR will be lower than $158m.

A statement in the annual report of a bank states that the 10-day VaR at the 95% level of confidence at the end of the year is $253m. Which of the following is true:

I. The maximum loss that the bank is exposed to over a 10-day period is $253m.

II. There is a 5% probability that the bank's losses will not exceed $253m

III. The maximum loss in value that is expected to be equaled or exceeded only 5% of the time is $253m

IV. The bank's regulatory capital assets are equal to $253m

According to the implied capital model, operational risk capital is estimated as:

Which of the following statements are true:

I. The three pillars under Basel II are market risk, credit risk and operational risk.

II. Basel II is an improvement over Basel I by increasing the risk sensitivity of the minimum capital requirements.

III. Basel II encourages disclosure of capital levels and risks

Which of the following statements is true in respect of a non financial manufacturing firm?

I. Market risk is not relevant to the manufacturing firm as it does not take proprietary positions

II. The firm faces market risks as an externality which it must bear and has no control over

III. Market risks can make a comparative assessment of profitability over time difficult

IV. Market risks for a manufacturing firm are not directionally biased and do not increase the overall risk of the firm as they net to zero over a long term time horizon

An asset has a volatility of 10% per year. An investment manager chooses to hedge it with another asset that has a volatility of 9% per year and a correlation of 0.9. Calculate the hedge ratio.

What ensures that firms are not able to selectively default on some obligations without being considered in default on the others?

The VaR of a portfolio at the 99% confidence level is $250,000 when mean return is assumed to be zero. If the assumption of zero returns is changed to an assumption of returns of $10,000, what is the revised VaR?

In the case of historical volatility weighted VaR, a higher current volatility when compared to historical volatility:

Under the basic indicator approach to determining operational risk capital, operational risk capital is equal to:

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that exactly 1 of the three bonds will default.

Which of the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. A correlation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

If two bonds with identical credit ratings, coupon and maturity but from different issuers trade at different spreads to treasury rates, which of the following is a possible explanation:

I. The bonds differ in liquidity

II. Events have happened that have changed investor perceptions but these are not yet reflected in the ratings

III. The bonds carry different market risk

IV. The bonds differ in their convexity

For a US based investor, what is the 10-day value-at risk at the 95% confidence level of a long spot position of EUR 15m, where the volatility of the underlying exchange rate is 16% annually. The current spot rate for EUR is 1.5. (Assume 250 trading days in a year).

The 10-day VaR of a diversified portfolio is $100m. What is the 20-day VaR of the same portfolio assuming the market shows a trend and the autocorrelation between consecutive periods is 0.2?

Which of the following statements are true:

I. It is usual to set a very high confidence level when estimating VaR for capital requirements.

II. For model validation, very high VaR confidence levels are used to minimize excess losses.

III. For limit setting for managing day to day positions, it is usual to set VaR confidence levels that are neither too low to be exceeded too often, nor too high as to be never exceeded.

IV. The Basel accord requirements for market risk capital require the use of a time horizon of 1 year.

The degree distribution of the nodes of the financial network is:

Under the CreditPortfolio View model of credit risk, the conditional probability of default will be:

Once the frequency and severity distributions for loss events have been determined, which of the following is an accurate description of the process to determine a full loss distribution for operational risk?

The unexpected loss for a credit portfolio at a given VaR estimate is defined as:

When pricing credit risk for an exposure, which of the following is a better measure than the others:

Financial institutions need to take volatility clustering into account:

I. To avoid taking on an undesirable level of risk

II. To know the right level of capital they need to hold

III. To meet regulatory requirements

IV. To account for mean reversion in returns

According to the Basel II framework, subordinated term debt that was originally issued 4 years ago with a maturity of 6 years is considered a part of:

A bank holds $10m of a corporate debt that it has purchased CDS protection against. What is the impact on the short term liquidity of the bank in the event of a default by the corporate on its bonds?

For an equity portfolio valued at V whose beta is ?, the value at risk at a 99% level of confidence is represented by which of the following expressions? Assume ? represents the market volatility.

Which of the following belong to the family of generalized extreme value distributions:

I. Frechet

II. Gumbel

III. Weibull

IV. Exponential

Who has the ultimate responsibility for the overall stress testing programme of an institution?

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

The definition of operational risk per Basel II includes which of the following:

I. Risk of loss resulting from inadequate or failed internal processes, people and systems or from external events

II. Legal risk

III. Strategic risk

IV. Reputational risk

Which of the following statements is true:

I. Basel II requires banks to conduct stress testing in respect of their credit exposures in addition to stress testing for market risk exposures

II. Basel II requires pooled probabilities of default (and not individual PDs for each exposure) to be used for credit risk capital calculations

Which of the following correctly describes survivorship bias:

Between two options positions with the same delta and based upon the same underlying, which would have a smaller VaR?

Which of the following are elements of 'group risk':

I. Market risk

II. Intra-group exposures

III. Reputational contagion

IV. Complex group structures

What does a middle office do for a trading desk?

If the annual variance for a portfolio is 0.0256, what is the daily volatility assuming there are 250 days in a year.

Which of the following credit risk models focuses on default alone and ignores credit migration when assessing credit risk?

Which of the following are true:

I. The total of the component VaRs for all components of a portfolio equals the portfolio VaR.

II. The total of the incremental VaRs for each position in a portfolio equals the portfolio VaR.

III. Marginal VaR and incremental VaR are identical for a $1 change in the portfolio.

IV. The VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than (or in extreme cases equal to) the sum of the individual VaRs.

V. The component VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than the sum of the individual component VaRs.

Random recovery rates in respect of credit risk can be modeled using:

What is the 1-day VaR at the 99% confidence interval for a cash flow of $10m due in 6 months time? The risk free interest rate is 5% per annum and its annual volatility is 15%. Assume a 250 day year.

For a loan portfolio, expected losses are charged against:

The sum of the stand alone economic capital of all the business units of a bank is:

3 Months Free Update

3 Months Free Update

3 Months Free Update

TESTED 19 Jul 2026